“It’s not what you earn; it’s what you keep.” This timeless adage hits home during tax season when every dollar counts.

Have you ever found yourself staring at your tax forms, wondering what’s the deal with tax credits vs tax deductions? Well, many taxpayers feel the same confusion.

After all, both sound like money saved—but they work in entirely different ways.

Let’s take a scenario of two neighbours who file their taxes.

One claims a $1,000 tax deduction, reducing their taxable income, while the other claims a $1,000 tax credit, slashing their tax bill directly.

and the result – they save very very differently.

So here is the catch you need to understand: Knowing these terms isn’t just IRS jargon—it’s your opportunity to maximise savings. From deductions that shrink taxable income to credits that directly cut taxes owed, today, we’re breaking down everything and defining the key differences so you’re ready to confidently take on your tax return.

Tax Credits vs Tax Deductions: Understanding the Key Differences

When it comes to reducing your tax liability, both tax credits and tax deductions can help, but they work in different ways. While they share some similarities, understanding how each affects your tax return is crucial for making the most of these benefits.

Let’s break down the differences and how they can impact your taxes.

Similarities Between Tax Credits and Tax Deductions

Both tax credits and tax deductions share a few common features:

- Eligibility Requirements: Both types of benefits come with specific requirements you must meet to qualify. These could be based on income, filing status, or other factors.

- State and Federal Options: Tax credits and tax deductions can be available at both the state and federal level. This means you might have access to tax benefits from both your state government and the federal government, depending on your situation.

Tax Credits vs Tax Deductions – Major differences

While both tax credits and tax deductions lower your overall tax burden, they do so in different ways.

- Tax Credit: A tax credit directly reduces the amount of tax you owe. If you qualify for a tax credit, the amount of the credit will be subtracted from your total tax bill. In other words, it lowers your tax bill dollar-for-dollar.

- Tax Deduction: A tax deduction reduces your taxable income. This is the amount of your earnings that are subject to tax. For example, if you earn $50,000 and have $5,000 in tax deductions, your taxable income becomes $45,000. The actual amount of tax you save depends on factors like your tax bracket.

How Do Tax Credits and Tax Deductions Impact Your Tax Return?

Let’s look at an example to clearly illustrate how each works.

- Tax Credit Example: If you owe $2,000 in taxes and qualify for a $500 tax credit, your tax bill is reduced by $500. You now only owe $1,500 in taxes. A tax credit is a straightforward way to reduce your taxes directly.

- Tax Deduction Example: If you have $5,000 in tax deductions and fall into a 25% tax bracket, your tax savings would be $1,250. This means that the $5,000 deduction reduces your taxable income, and your taxes owed decrease by 25% of that amount.

Whether you qualify for credits or deductions (or both), they can significantly lower the amount of taxes you owe.

Tax Credits vs. Tax Deductions: How They Impact Your Tax Bill in 2025

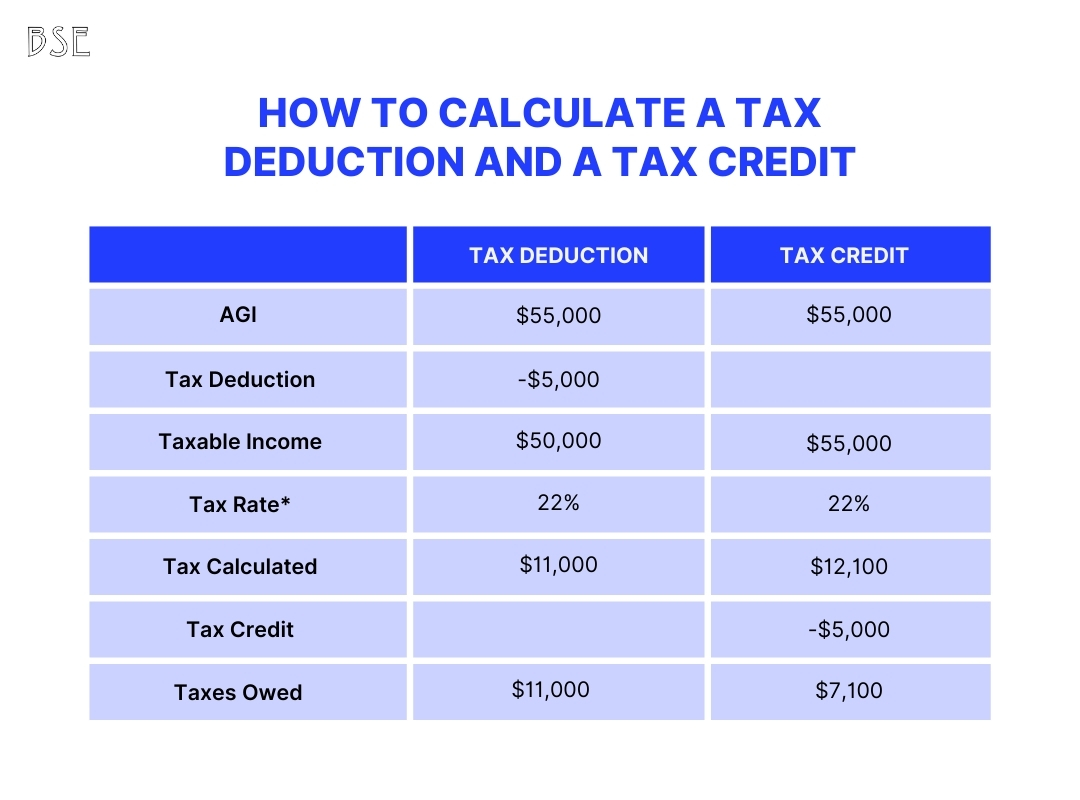

Now that we’ve covered the definitions of tax credits and tax deductions, it’s time to look at how each affects your tax bill. To give you a clearer picture, let’s explore an example with an Adjusted Gross Income (AGI) of $50,000 and compare the impact of a $10,000 tax credit versus a $10,000 tax deduction.

Tax Deduction Example

A tax deduction reduces your taxable income. Let’s say your AGI is $55,000, and you apply a tax deduction of $5,000. The $5,000 deduction reduces your taxable income from $55,000 to $50,000.

Here’s how that works:

- AGI: $55,000

- Tax Deduction: -$5,000

- Taxable Income: $50,000

- Tax Rate: 22% (assuming the 2024 tax brackets)

When your taxable income is reduced to $50,000, you’re taxed on that amount, and the calculation comes to $11,000 in taxes owed.

Tax Credit Example

In contrast, a tax credit works differently. It directly reduces the amount of taxes owed rather than lowering your taxable income. So, if you have a tax credit of $10,000, it’s applied to your total tax bill.

Here’s the breakdown:

- AGI: $55,000 (same as in the tax deduction example)

- Taxable Income: $55,000 (no change in this case, as the tax credit does not affect taxable income)

- Tax Rate: 22%

- Tax Calculated: $12,100 (calculated as 22% of $55,000)

Then, you apply the $10,000 tax credit directly to your tax bill. The taxes owed after applying the credit would be $7,100 ($12,100 – $10,000).

Comparison

- Taxes Owed with Tax Deduction: $11,000

- Taxes Owed with Tax Credit: $7,100

As you can see, in this example, the tax credit reduces your taxes owed by more than the tax deduction. This highlights one of the key advantages of tax credits—they provide more direct relief by reducing the amount of tax you need to pay, rather than just lowering your taxable income.

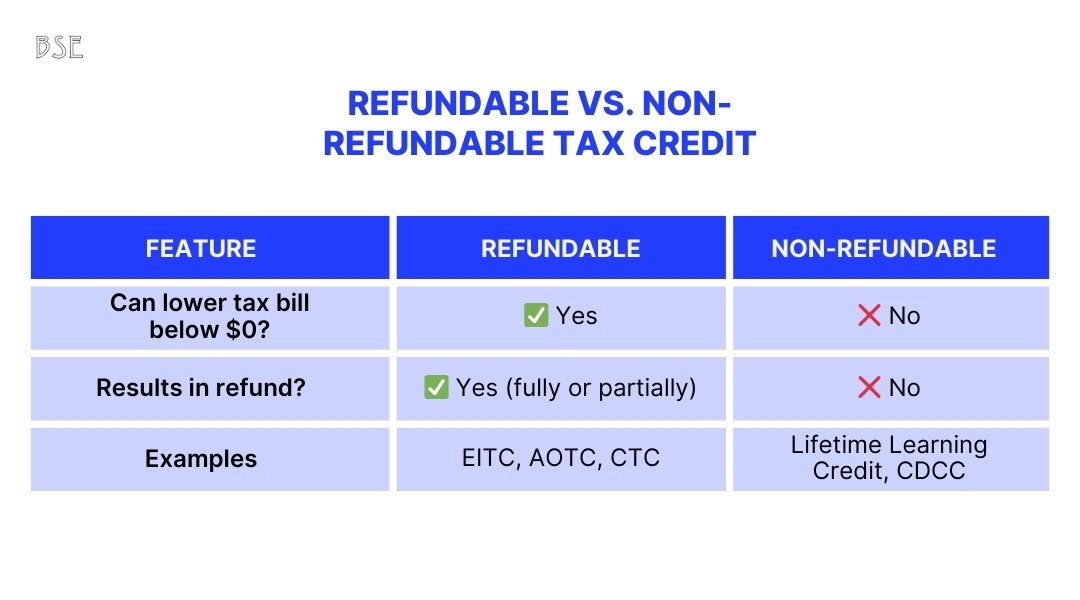

Refundable vs. Non-Refundable Tax Credits: What’s the Difference?

When you’re looking to reduce your taxes, one key factor to understand is the difference between refundable and non-refundable tax credits. These two types of credits can affect your tax refund and the overall amount of taxes you owe.

a. Refundable Tax Credits

Refundable tax credits are the more beneficial option if you want a refund. This means that if the credit reduces your tax liability to zero and there’s still money left, you may receive the remaining amount as a refund. For example, if you owe $500 in taxes but qualify for a $1,000 refundable credit, the IRS will refund you $500.

One popular example of a refundable tax credit is the Child Tax Credit (CTC). The federal portion of this credit is partially refundable, meaning it can reduce your tax liability below zero and lead to a refund, depending on your income level and other factors. The refundable portion is adjusted annually for inflation, making it a valuable tool for many taxpayers, especially those with children under 17.

b. Non-Refundable Tax Credits

On the other hand, non-refundable tax credits do not offer a refund. If your credit exceeds your total tax liability, the remaining amount is simply not applied. For example, if you qualify for a $1,000 non-refundable credit but only owe $800 in taxes, you can only use $800 of the credit. The remaining $200 is not refunded.

While non-refundable credits may not provide a refund, they can still be beneficial by reducing your taxable income and lowering the amount you owe. Common examples include education-related credits or certain energy-efficiency credits.

c. Partially Refundable Tax Credits

In some cases, tax credits are partially refundable, meaning only a portion of the credit may be refunded to you if it exceeds your tax liability. This allows taxpayers to receive a refund for a portion of the credit while still benefiting from the rest to reduce their tax obligation. The Earned Income Tax Credit (EITC) is another well-known partially refundable credit that helps low- to moderate-income taxpayers.

d. Eligibility and Income Limits

Both refundable and non-refundable tax credits have eligibility requirements. These can include income limits, filing status, and specific criteria for the credit itself. For example, the amount you can receive from the Child Tax Credit or the EITC depends on your income and the number of qualifying children.

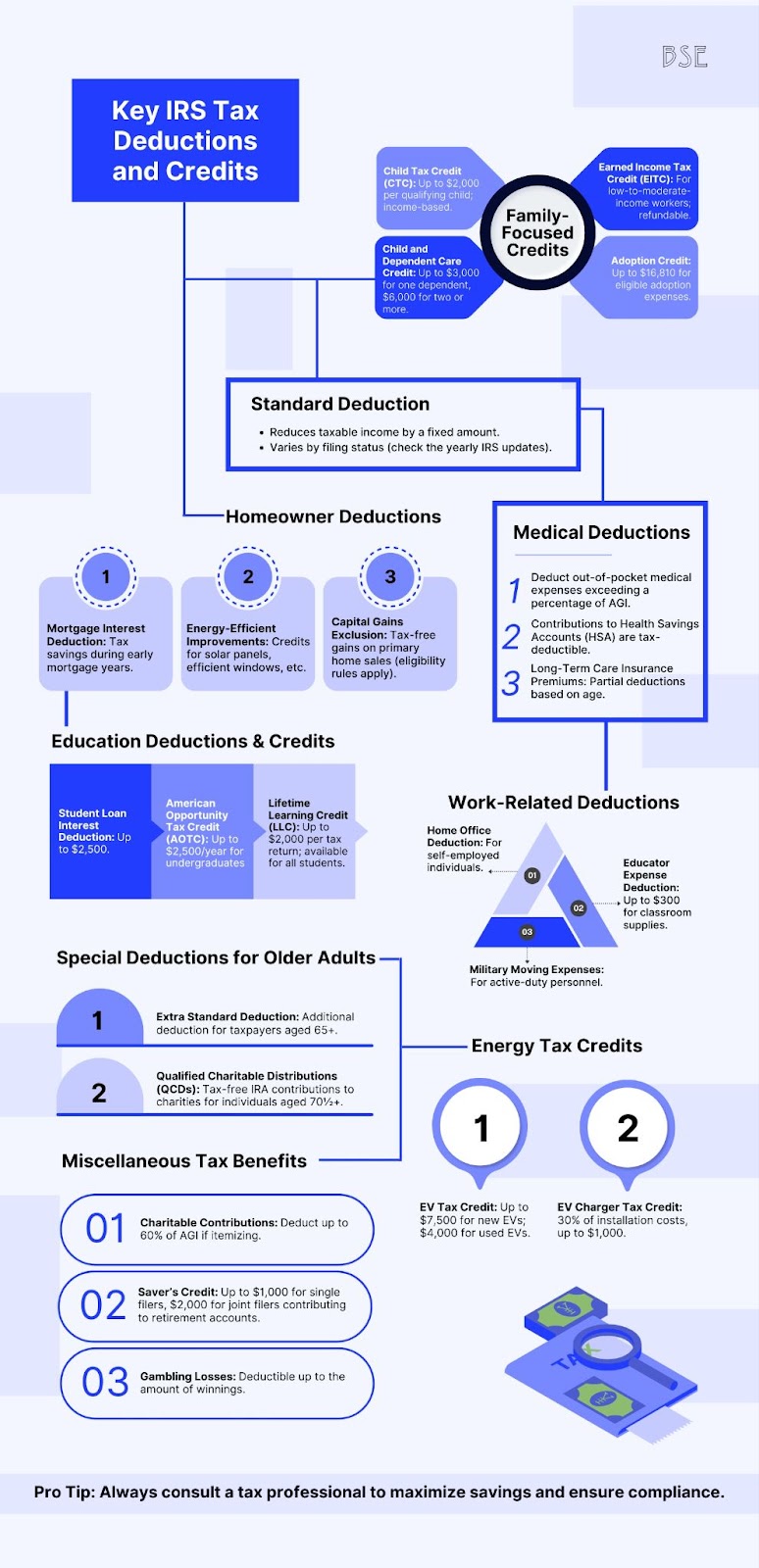

Common Tax Credits You May Be Eligible For

Unlike tax deductions, which reduce your taxable income, tax credits reduce the actual amount of taxes you owe. Here’s a closer look at some of the most common tax credits:

1. Earned Income Tax Credit (EITC)

The Earned Income Tax Credit (EITC) is designed to help low- to moderate-income workers. It’s a refundable credit, meaning if your tax liability is less than your credit, you could get the difference back as a refund. For example, if you qualify for a $1,500 EITC but only owe $1,000 in taxes, the IRS will send you the $500 difference. The amount you can claim depends on your income, filing status, and number of children.

For 2025, the credit can range from a few hundred dollars to over $6,000 for families with children. Even if you don’t have children, you may still qualify for a smaller credit.

2. Child Tax Credit (CTC)

If you have children under age 17, the Child Tax Credit (CTC) could give you up to $2,000 per child. The key thing to know about this credit is that $1,400 of that $2,000 is refundable. This means that even if you don’t owe much in taxes, you could still receive up to $1,400 for each qualifying child.

For example, if you owe $500 in taxes but qualify for the full $2,000 credit, you could get a $1,500 refund. This makes the CTC especially beneficial for parents.

3. Electric Vehicle (EV) Tax Credit

If you bought a new electric vehicle (EV), you might be able to claim an EV Tax Credit. This credit can be as much as $7,500, but it depends on the make and model of the car. The credit is nonrefundable, so it can only reduce the taxes you owe, not result in a refund. Keep in mind that the credit is subject to income and vehicle price limits.

For instance, if you buy an electric car that’s too expensive or if your income is above a certain threshold, you might not qualify for the full credit. Always check the latest IRS guidelines to make sure your vehicle qualifies.

4. Federal Tax Credits for Homeowners

If you’ve made energy-efficient upgrades to your home, like installing solar panels or energy-efficient windows, you may be able to claim tax credits for those improvements.

For example, the Residential Energy Efficient Property Credit allows you to claim a percentage of the cost of solar panels and certain other renewable energy systems.

In 2025, this credit can cover up to 30% of the cost of installing solar energy systems. This can help reduce your tax liability and make these upgrades more affordable.

5. Education Tax Credits

Education expenses can be a big burden, but there are tax credits to help offset those costs. The American Opportunity Tax Credit (AOTC) provides up to $2,500 per student for qualified education expenses like tuition, fees, and books.

Half of the AOTC is refundable, so if you don’t owe much in taxes, you could still receive up to $1,250 back. This credit can be claimed for each of the first four years of higher education.

Another option is the Lifetime Learning Credit, which offers up to $2,000 per tax return for qualified educational expenses. It’s not as large as the AOTC, but it applies to a broader range of educational levels, including graduate school.

Above-the-Line Deductions: How They Can Help You Save Without Itemizing

When it comes to reducing your taxable income, most people focus on either taking the standard deduction or itemizing their deductions. However, there’s another important type of tax deduction called “above-the-line” deductions. These deductions can be especially useful because you don’t need to itemize your deductions to benefit from them.

Above-the-line deductions are subtracted directly from your gross income, lowering your Adjusted Gross Income (AGI). This means they reduce your taxable income before calculating your tax liability, which can lead to a lower overall tax bill.

Here are some of the most common above-the-line tax deductions available:

- Contributions to an IRA or Health Savings Account (HSA): If you contribute to a traditional IRA or an HSA, you can deduct those contributions from your gross income. This can help you save for retirement or cover medical expenses while lowering your taxable income in the current year.

- Educator Expense Deduction: Teachers and eligible educators can deduct up to $300 (or $600 for married couples filing jointly) for unreimbursed expenses they incur for classroom supplies and other eligible teaching materials.

- Student Loan Interest Deduction: If you’re paying off student loans, you may be able to deduct up to $2,500 of the interest you pay on those loans. This deduction is available even if you don’t itemize your deductions.

Key Points to Remember About Above-the-Line Deductions

- No Need to Itemize: Unlike itemized deductions, which require you to track a variety of expenses like medical bills or charitable donations, above-the-line deductions don’t require any additional paperwork or complexity.

- Eligibility Criteria: Some of these deductions, such as the student loan interest deduction, may be subject to income limits. It’s important to check that you meet the eligibility requirements before claiming them.

- Impact on AGI: Since above-the-line deductions directly reduce your AGI, they can also have an impact on other tax benefits tied to your AGI, such as eligibility for tax credits.

In the next section, we’ll shift focus to the more commonly discussed “below-the-line” deductions, comparing itemized versus standard deductions to help you decide the best approach for your tax situation.

Itemized Deductions: What You Need to Know

After you’ve considered your above-the-line deductions, it’s time to focus on your below-the-line deductions. These deductions come into play after calculating your Adjusted Gross Income (AGI) and can have a significant impact on your tax bill.

You’ll have the option to choose between taking the standard deduction or itemizing your deductions, but you can’t do both.

For many taxpayers, itemizing deductions can be the key to reducing taxable income further. If your itemized deductions exceed the standard deduction amount, you’ll want to claim them instead.

Here are some common types of itemized deductions that might apply to you:

a. Charitable Contributions

Donating to qualified charities is one way to lower your taxable income. Whether it’s cash or goods, these donations can often be deducted from your taxes.

b. Property Tax

If you own a home, the property taxes you pay can often be deducted from your total income. This can be particularly beneficial in high-tax states.

c. Mortgage Interest

Homeowners can generally deduct the interest paid on their mortgage for their primary residence. This deduction can help reduce the overall cost of owning a home.

d. Gambling Losses

If you’ve had a lucky streak at the casino or gambling establishment, it’s important to note that you can deduct gambling losses, but only to the extent of your gambling winnings. This deduction can be a helpful way to offset your taxable income if you’ve had a successful year in gambling.

e. Medical Expenses

You may be able to deduct medical and dental expenses if they exceed a certain percentage of your AGI. This can be a valuable deduction if you’ve had significant medical costs throughout the year.

When deciding whether to take the standard deduction or itemize, it’s a good idea to consult with a tax professional. They can help you determine which option offers the most significant savings based on your specific circumstances.