As we approach mid-December, it’s natural to reflect on the past year. From global conflicts and lower interest rates to the election of a new president and the U.S. market hitting all-time highs, 2024 had its fair share of major headlines. While it’s easy to get caught up in the latest news, focusing solely on short-term events may not be the best approach.

With the clock ticking down to December 31st, the final weeks of the year are a prime time for tax planning. By taking a proactive approach now, you can leverage several strategies that may save you big.

Here are 20 year-end tax planning strategies to consider before the year ends.

1. Assess Your Investment Allocation

With market shifts, it’s crucial to review how your investments are spread across different asset classes—stocks, bonds, real estate, and cash. Your goals may have changed, and so should your portfolio.

Make sure that your investment allocation still aligns with your risk tolerance and long-term objectives. If you’ve had major life changes, like a new job, a house purchase, or a shift in financial priorities, now’s the time to ensure your portfolio reflects those changes.

A diversified investment strategy can help protect against market volatility and provide long-term growth, but it’s essential that your mix of assets remains in sync with your financial goals as you approach 2025.

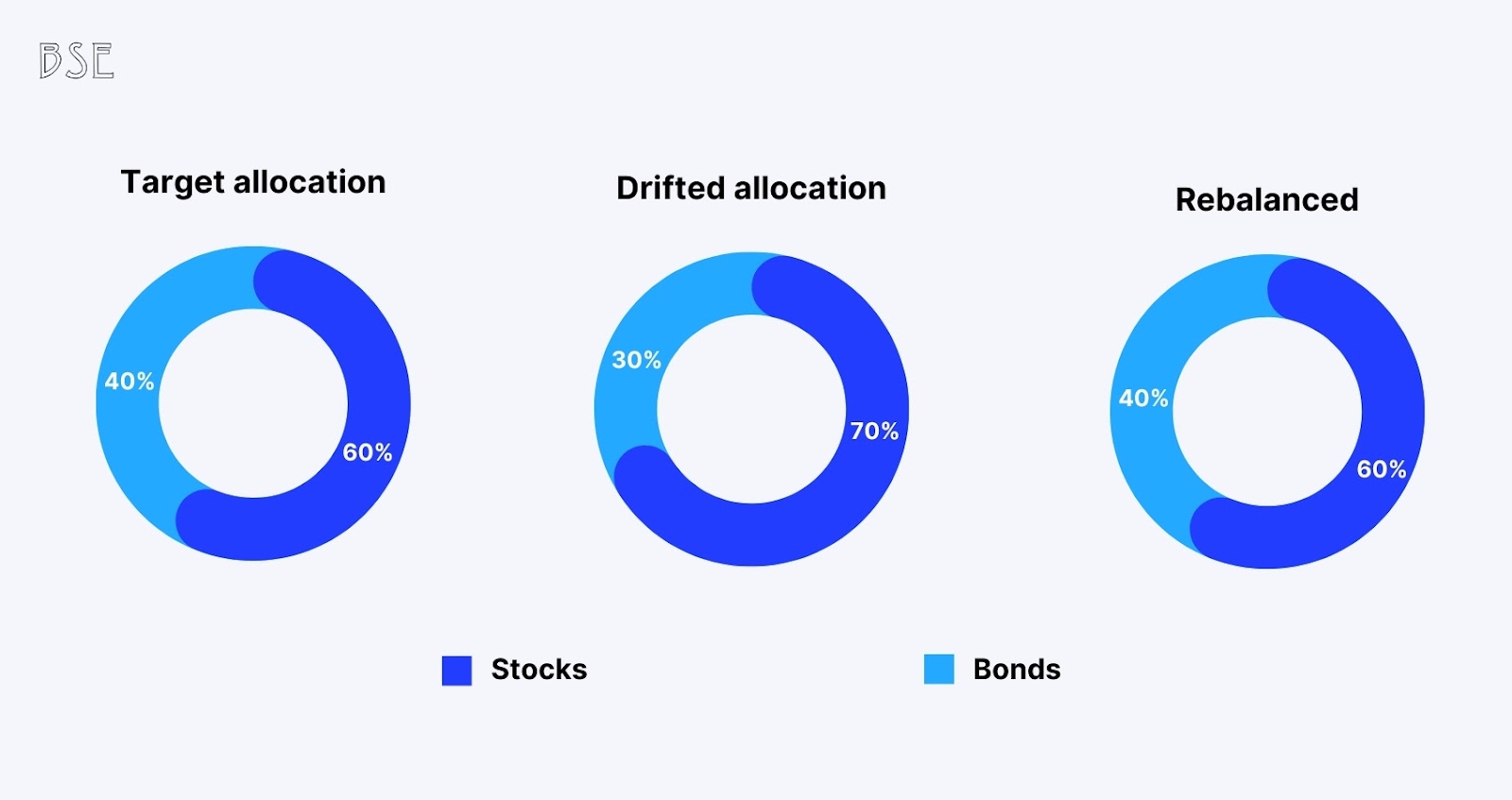

2. Rebalance Your Portfolio

If your portfolio has drifted from its intended allocation—especially with the tech stocks leading the market this year—it might be time for a rebalance.

The S&P 500 has been largely driven by a few large tech companies, but other areas, such as international stocks, REITs, and bonds, have underperformed. This might mean your portfolio has become skewed, with some areas overexposed to growth while others are lagging.

Rebalancing your portfolio ensures that you return to your desired risk profile. Rebalancing can help you lock in gains in the top-performing sectors, while buying more of the underperforming sectors that could recover.

Regularly adjusting your portfolio can help you maintain a balanced risk exposure and stay on track with your long-term investment objectives.

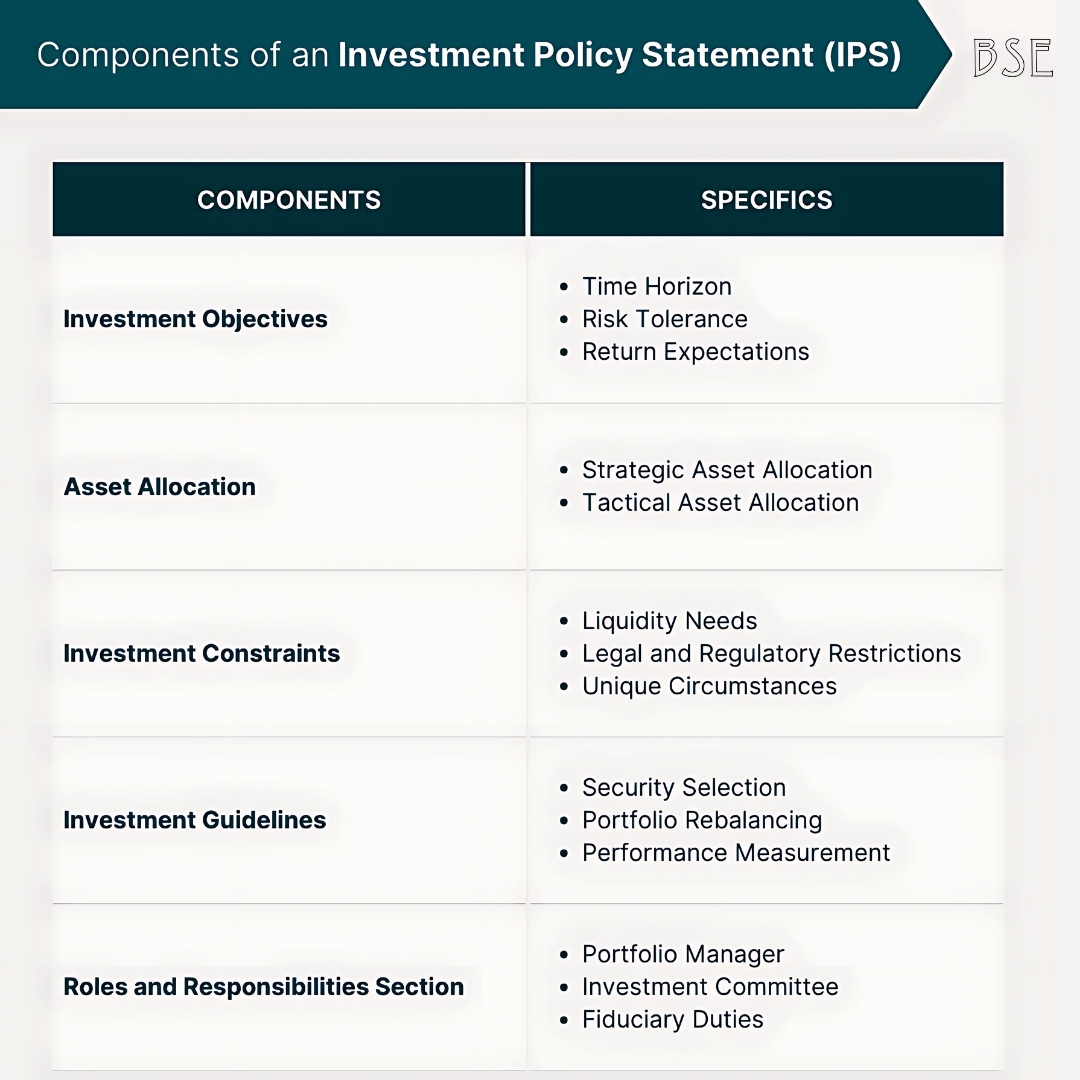

3. Set Up an Investment Policy Statement (IPS)

One of the best ways to stay disciplined in your investing is to create an Investment Policy Statement (IPS). This document outlines your financial goals, risk tolerance, and the specific strategies you’ll follow to meet your objectives.

It provides clarity and helps keep your investments on track. Without an IPS, it’s easy to get distracted by market noise or salespeople pushing investments that don’t fit your strategy.

Developing and updating an IPS with your financial advisor before the year ends will ensure that you enter 2025 with a clear investment approach. It’s a valuable tool that can keep you focused on your goals and prevent impulsive decisions that might harm your portfolio’s long-term success.

4. Review Your Cash Position

While cash might not be a star performer in terms of returns, it still plays a vital role in your financial stability.

With money market yields hovering around 4%, it’s wise to move your cash from low-yield accounts to higher-yielding options. Many accounts offer interest rates well below the current market average, which could mean you’re missing out on earning extra income.

Additionally, while cash should always be available for emergencies, you don’t want to hold too much. Consider evaluating how much cash you need for short-term goals, and make sure you’re optimizing it to work for you.

If you haven’t done so already, look for higher-yielding accounts that offer a better return on your idle funds.

5. Don’t Forget Required Minimum Distributions (RMDs)

For those 73 or older, it’s important not to forget about Required Minimum Distributions (RMDs).

These mandatory withdrawals from retirement accounts like IRAs and 401(k)s come with penalties if not taken by December 31. If you’re subject to RMDs, make sure to schedule and take your distributions before the year ends.

These withdrawals are taxable, but if you fail to take them, you could face a penalty of 50% on the amount you were required to withdraw.

By staying on top of RMDs, you can avoid unnecessary penalties and ensure that you’re meeting the IRS requirements for your retirement accounts.

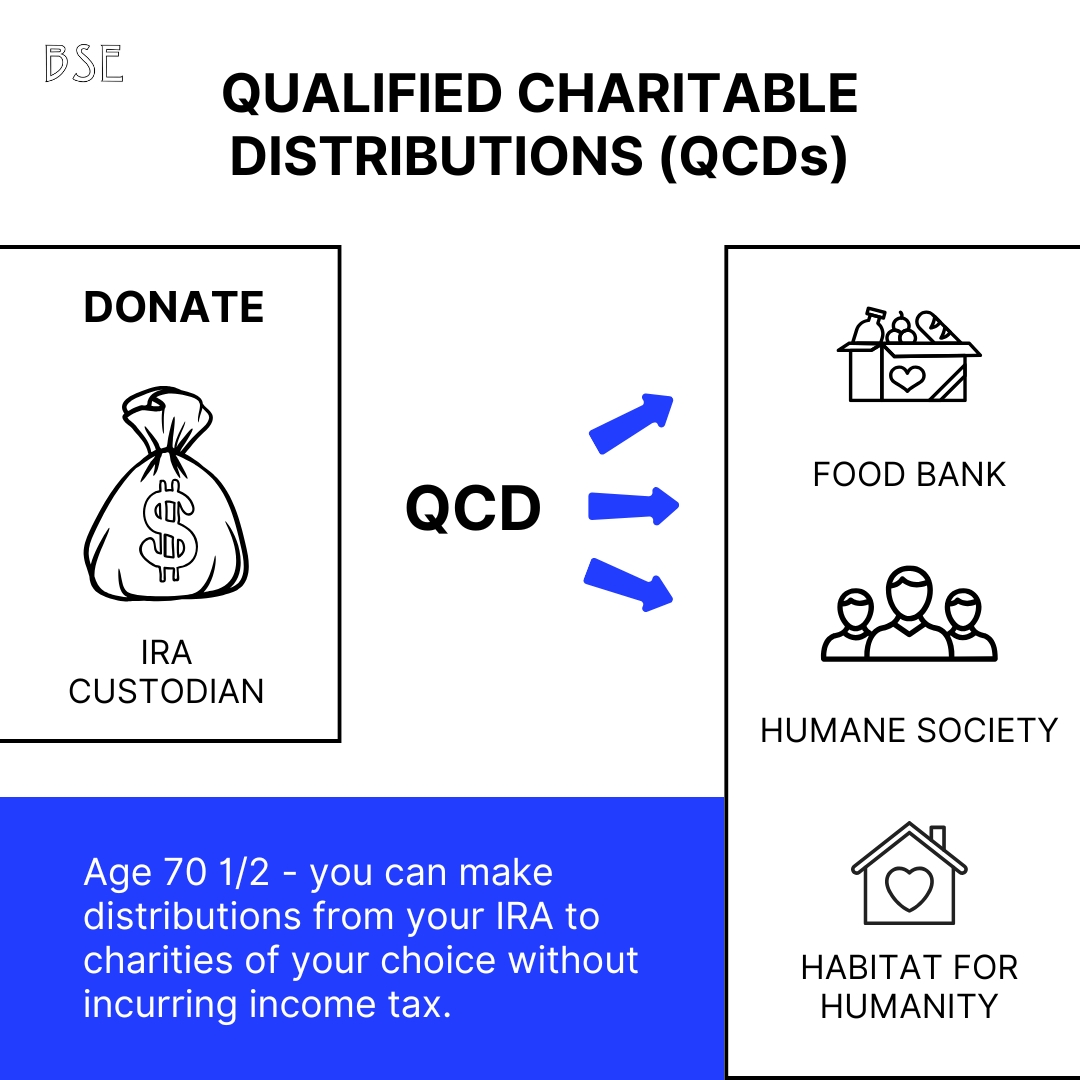

6. Leverage Qualified Charitable Distributions (QCDs)

If you’re 70½ or older, you can donate a portion of your Required Minimum Distribution (RMD) directly to a charity through a Qualified Charitable Distribution (QCD).

This is a smart way to give to charity while reducing your taxable income. In 2024, you can donate up to $105,000 from your IRA to qualifying charities without having to pay tax on those funds.

A QCD is an efficient way to fulfill your charitable giving goals while also helping to manage your tax liability. This is particularly valuable in years when you’re subject to RMDs and want to give back while reducing your taxable income.

Consider using QCDs to make a meaningful impact in your community while benefiting from tax savings.

7. Maximize Your Charitable Contributions

If you’re planning to donate to charity, now is a great time to consider maximizing your gifts.

Under the Tax Cuts and Jobs Act, the deduction for cash contributions to charity has increased from 50% to 60% of your Adjusted Gross Income (AGI). However, this benefit will revert back to 50% after 2025, so it’s worth making your charitable contributions now to take advantage of this higher deduction.

Whether you donate cash or through a donor-advised fund, you can make a larger impact this year. Charitable giving can be a win-win, allowing you to contribute to causes you care about while reducing your taxable income for the year.

8. Donate Appreciated Stocks

For those holding long-term investments with significant capital gains, donating appreciated stocks can be a powerful way to reduce your tax burden.

By donating these securities directly to a charity, you avoid paying capital gains taxes on the appreciation. Not only does this allow you to support a cause you care about, but it also helps to de-risk your portfolio by reducing the size of a concentrated position.

This strategy is particularly valuable for individuals with large, appreciated positions in stocks or other securities. It helps you meet your charitable goals while minimizing tax liabilities—something to consider if you’re looking to manage your portfolio’s risks and give back before year-end.

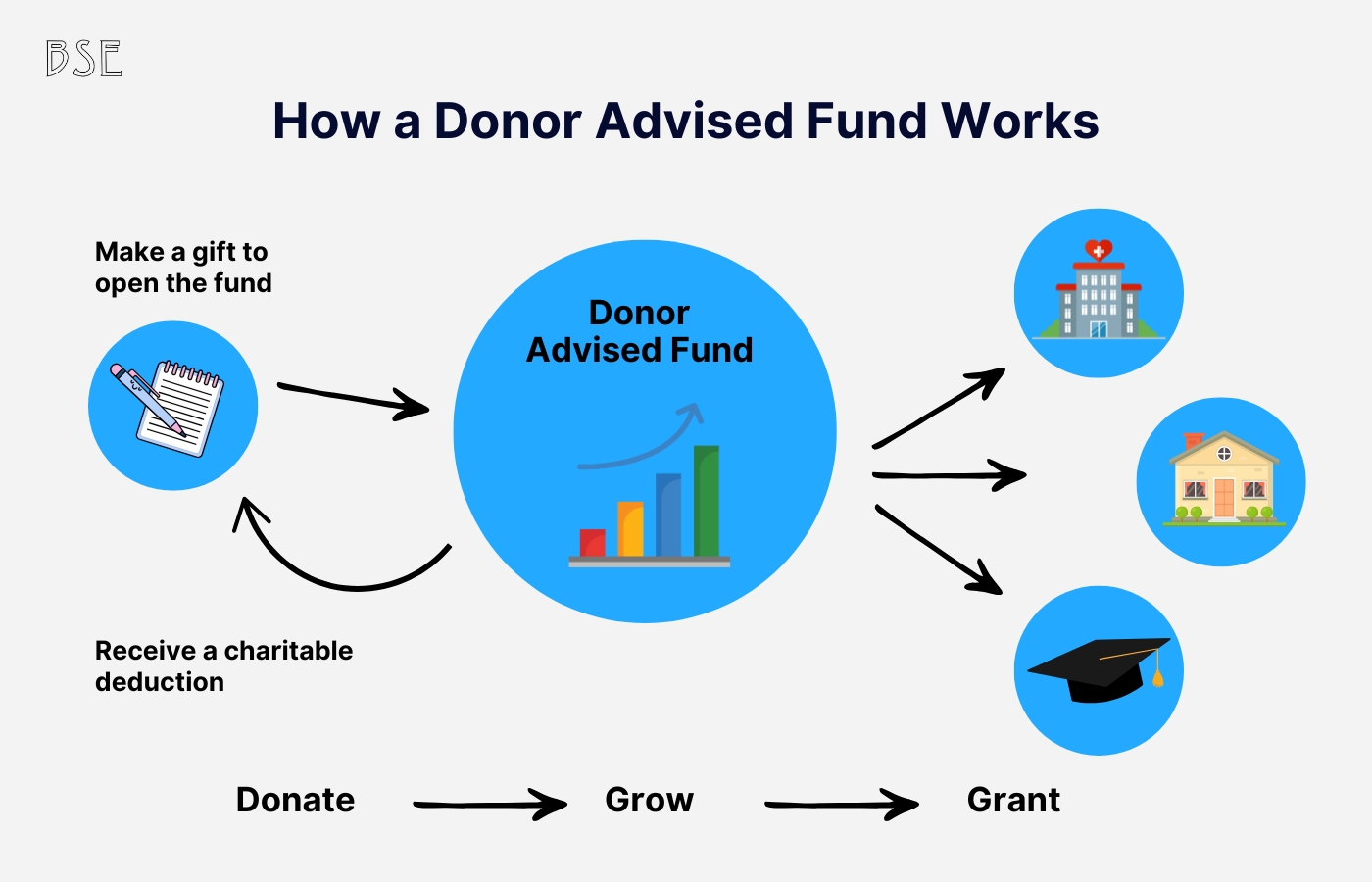

9. Use a Donor-Advised Fund (DAF)

A Donor-Advised Fund (DAF) offers a flexible way to manage your charitable giving. When you contribute to a DAF, you receive an immediate tax deduction for the year.

You can then decide when and how the funds are distributed to various charities. This is an excellent strategy if you have highly appreciated securities or concentrated stock positions. Instead of selling them and triggering capital gains taxes, you can move those assets to the DAF, avoiding those taxes while still benefiting from a tax deduction.

Additionally, DAFs allow you to “bunch” charitable contributions, which means donating several years’ worth of gifts at once to take advantage of tax planning opportunities. It’s an efficient way to plan your giving while maximizing tax savings.

10. Consider a Roth IRA Conversion

Converting a traditional IRA or 401(k) into a Roth IRA can be a beneficial strategy, particularly for tax planning. When you convert, you pay income taxes on the funds at the time of conversion, but future growth and withdrawals are tax-free.

This can help you avoid a higher tax burden in retirement or leave a more tax-efficient legacy. Roth conversions are especially beneficial if you expect your tax rate to be higher in the future. However, it’s essential to plan for the tax impact of the conversion.

In some cases, spreading the conversion over multiple years can help reduce the immediate tax hit. This strategy can be a useful tool for both long-term growth and estate planning.

11. Review Beneficiary Designations

Even if you’ve done estate planning and have a will in place, it’s essential to review your beneficiary designations for retirement accounts, life insurance policies, and other assets.

These designations override any instructions in your will, so it’s important to ensure they reflect your current wishes.

For example, if you’ve gone through a divorce or have had a change in family dynamics, you may need to update your beneficiaries. Failing to do so could result in unintended individuals receiving your assets, such as an ex-spouse.

A quick review of these designations can help avoid potential issues in the future and ensure your assets are distributed according to your desires.

12. Update Your Estate Plan for Changing Family Dynamics

Life changes, especially with the loss of a loved one, can significantly affect your estate planning needs.

If there has been a death in the family, it’s a good idea to consult with an estate planning attorney to ensure your documents are up to date. Wills, powers of attorney, and health care proxies should be reviewed to reflect any changes in your family structure.

It’s also a good time to consider whether your current plan aligns with your financial goals and asset distribution preferences. Keeping your estate plan current ensures that your wishes are respected and that your family is well taken care of, no matter what happens.

13. Use the High Estate and Gift Tax Exemption

The estate and gift tax exemption for 2024 is at an all-time high, allowing individuals to give up to $13.61 million and married couples up to $27.22 million without triggering estate taxes.

This amount is set to increase slightly next year, but it’s important to note that the exemption is scheduled to drop in 2026 unless new legislation is passed. If you have significant assets, now might be the time to take advantage of the high exemption to make large gifts or transfers without incurring tax liabilities.

This can help you reduce the size of your estate and transfer wealth to your heirs while avoiding future tax burdens.

14. Contribute to a 529 College Savings Plan

If you have children or grandchildren, contributing to a 529 plan is a smart move. These tax-advantaged accounts allow you to save for college expenses while receiving tax deductions in some states.

If you live in a state with a state tax deduction for contributions, it’s worth contributing before the year ends to maximize your savings. In 2024, you can gift up to $18,000 per person without triggering gift taxes, and if you’re married, that amount doubles.

Additionally, you can “superfund” a 529 plan, meaning you contribute up to $180,000 in a single year, as long as you spread the gift over five years for gift tax purposes.

15. Utilize Tax-Loss Harvesting

Tax-loss harvesting is a strategy that allows you to offset capital gains with losses, reducing your overall tax liability.

If you have investments that are currently at a loss, consider selling them before the end of the year to lock in those losses. These losses can be used to offset gains from other investments, which can reduce your taxable income.

If you’ve had a particularly strong year in the stock market, tax-loss harvesting can help mitigate some of the tax burdens by reducing the capital gains tax you owe.

It’s a great way to lower your tax bill while maintaining a balanced investment portfolio.

16. Maximize Retirement Contributions

Contributing to retirement accounts like a 401(k) or IRA is one of the most effective ways to grow your wealth while taking advantage of tax breaks. For 2024, the contribution limit for a 401(k) is $23,000 (or $30,000 if you’re 50 or older), and for an IRA, it’s $6,500 (or $7,500 for those 50 and older).

If you haven’t yet maximized your contributions for the year, making the most of these limits before the end of December can provide a significant boost to your retirement savings. Beyond growing your wealth, contributions to traditional retirement accounts also reduce your taxable income, which can help lower your current tax liability.

Remember, if you haven’t set up automatic contributions, now is the time to do so to ensure you reach the maximum contribution limit.

17. Take Advantage of Health Savings Accounts (HSAs)

If you have a high-deductible health plan (HDHP), contributing to a Health Savings Account (HSA) can be a fantastic strategy for both health care expenses and long-term growth.

For 2024, the contribution limit for an HSA is $3,850 for individuals and $7,750 for family coverage (with an additional $1,000 catch-up contribution if you’re 55 or older). HSAs offer a triple tax benefit: contributions are tax-deductible, the account grows tax-free, and withdrawals for qualified medical expenses are tax-free as well.

Contributing to an HSA before the end of the year is an excellent way to reduce your taxable income while building a nest egg for future medical expenses. Additionally, funds in the HSA roll over from year to year, allowing you to accumulate savings for future health care needs.

18. Consider a Tax-Efficient Withdrawal Strategy

If you’re already in retirement or close to it, having a strategy for withdrawing money from your retirement accounts is crucial for minimizing taxes. A well-thought-out withdrawal strategy takes into account the tax implications of different accounts—such as 401(k)s, IRAs, and Roth IRAs—so you can minimize your overall tax bill over time.

For example, consider withdrawing funds from taxable accounts first, followed by tax-deferred accounts, and leaving tax-free Roth IRAs for last. This approach allows your tax-deferred accounts to continue growing without being taxed until later.

Working with a financial advisor to implement a tax-efficient withdrawal strategy can significantly improve your retirement income and reduce the taxes you’ll owe over time.

19. Evaluate Your Insurance Coverage

As you move through different stages of life, your insurance needs change. Now is the time to review your life, health, and property insurance policies to ensure they still meet your needs.

If you’ve had major life events like marriage, the birth of children, or purchasing a home, updating your insurance coverage is essential. Consider whether your current life insurance policy provides enough coverage for your loved ones, and whether your auto or homeowner’s insurance needs adjustment.

Additionally, review your health insurance plan to ensure it offers the best coverage for your medical needs. Evaluating your insurance coverage annually can save you money, avoid unnecessary gaps in coverage, and ensure you’re properly protected in case of an unexpected event.

20. Plan for Next Year’s Tax Strategy

As the year draws to a close, it’s a good time to start planning your tax strategy for the next year.

By projecting your income, deductions, and credits, you can estimate your potential tax liability and make adjustments to reduce what you owe. This could involve strategically timing income and deductions, taking advantage of tax credits, or changing the way you invest in tax-deferred accounts.

In particular, if you anticipate significant changes in income, such as a raise, a bonus, or a sale of assets, planning ahead can help you adjust your strategy. Additionally, staying up to date with any potential changes to tax laws can provide you with new opportunities to minimize taxes.

Having a proactive approach to your tax strategy ensures that you’re always a step ahead of the IRS.

ALSO READ – Tax Credits vs Deductions: How to Reduce Taxes Like a Pro in 2025