Do you know how some rich folks keep getting richer? Well, one trick they use is called tax avoidance.

So, the top 1% of rich households in the U.S. owned about 23.3% of the country’s money in 2023. That’s more than the 22.8% they had the year before. Surprisingly, the IRS says these guys only pay around 26% in taxes on average.

Now, tax avoidance is legal (unlike tax evasion which can land you in jail). It’s a smart strategy anyone can use to cut down on taxes. All you need to do is understand and use some popular loopholes that the wealthy exploit. Check out these 12 ways to save more on your taxes.

How much do rich people avoid in taxes annually?

The wealthiest 1% in the United States reportedly underpay their taxes by $163 billion each year, according to U.S. Treasury estimates.

The super-rich employ various methods to minimize tax payments:

- Foundations

- Property

- Gifting

- Family offices

- Investments

- Moving residency

These methods allow the top 1% to navigate tax obligations in a way that reduces their annual payments.

Now here are 12 super ways how you can save more on your taxes by using the right strategies-

#1. Depreciation –

So, depreciation is this cool trick the wealthy use to save on taxes. Here’s the scoop: it’s a deduction that helps you recover the cost of certain stuff for your federal income taxes. According to tax whiz Kelly Phillips Erb, you start depreciating something when you’re ready to use it, not necessarily when you actually use it. They call this “placing it in service.”

Now, depreciation isn’t picky – it works for both tangible and intangible things like buildings, rental spots, machines, cars, furnishings, patents, copyrights, and some software. But there are three rules: it has to be used for business or making money, you’ve got to own it, and it needs to last more than a year.

When it comes to claiming this magic deduction, it’s all in section 179 of your federal tax returns. For the 2023 tax year, you could snag a max deduction of $1,160,000 for most stuff. And guess what? For 2024, it’s bumped up to $1,220,000.

#2. Business Expenses Deductions

To claim tax deductions for business expenses, business owners must be aware of qualifying factors. Deductions can be made for various expenditures related to travel, vehicles, office supplies, work-related education, and a home office. It is crucial to differentiate between a legitimate business and a mere hobby, as only the former qualifies for tax benefits.

The IRS evaluates several factors to distinguish between a hobby and a bona fide business. These factors include maintaining proper records, conducting the activity in a businesslike manner, demonstrating intent to make a profit through time and effort, relying on the activity for livelihood, and assessing the profitability of the business over time.

#3. Employ Your Children/Kids

If you involve your family in your business, it can save you money. Hiring your kids to do real work in your business comes with potential tax advantages.

When it comes to partnerships and sole proprietorships owned by a child’s parents, the IRS states that payments for a child’s services under 18 are not subject to Social Security and Medicare taxes.

Moreover, your kids won’t be taxed on their income unless it goes beyond the standard deduction. For tax year 2023, the standard deduction is $13,850, and for tax year 2024, it’s $14,600.

There’s an extra tax benefit when you put your kids to work in your business: you can deduct their wages as a business expense.

To claim this deduction, instead of paying high taxes on your business income, transfer some of that income to your child as wages for the services they provide. It’s essential that your child’s work is legitimate, and the salary must be reasonable.

#4. Utilize Business Losses Wisely

Business owners, including the rich ones also, sometimes face losses. However, there’s a helpful IRS rule called “net operating loss carryforward.” This rule enables business owners to carry forward losses from a year to a future when the deduction would be more beneficial.

Business losses, often referred to as net operating losses (NOL), occur when tax deductions exceed taxable income. This can create an imbalance, especially if there were positive taxable income in other years resulting in taxes payable. The NOL serves to rectify this by allowing you to use the loss in one year to lower taxable income and reduce the tax burden in another year.

To claim this deduction:

- For tax years 2018 through 2020, the IRS permitted NOL carrybacks. This meant carrying back the entire NOL amount for up to five years. If there was still an NOL remaining after carrying those losses back, you could then carry the losses forward.

- Starting from tax year 2021, most businesses can only carry losses forward. This implies applying the loss towards your income in a future year.

#5. Building Wealth Through Smart Investments

Earn money through investments, not your job. Instead of working for your income, let your money work for you.

Consider investments like real estate investment trusts (REITs) and master limited partnerships (MLPs). These are structured to provide a steady income through distributions. You can also explore options like investing in stocks or purchasing rental properties for real estate investment. Keep in mind that significant upfront investments are necessary, and returns are not guaranteed.

To save on taxes, focus on high-yielding dividend stocks. Collect regular dividends and, later, sell the stock at a relatively low capital gains tax rate when it appreciates. Long-term capital gains tax rates are currently 0%, 15%, and 20% based on earnings in a particular year.

If you own rental property, deduct your property taxes. However, ensure you find responsible tenants who pay rent on time and take care of your property. Keep in mind that unexpected repairs and periodic improvements can be costly.

#6. Sell the Inherited Real Estate Wisely

Sell inherited real estate to minimize capital gains taxes. When you inherit property, take advantage of the “step-up in basis.” If you buy land for $200,000 and sell it for $450,000, you owe tax on the $250,000 gain. But if you inherit the land purchased for $200,000, your new basis is the property’s fair market value at the time of inheritance. If you sell it immediately, you won’t owe tax on the $250,000 gain.

This deduction is also automatic when property passes through inheritance. It’s like starting fresh, buying the property at the current value. For instance, if you inherit from your parents, there’s no capital gains tax on the $250,000 increase when you sell with the step-up basis. Avoid having your parents give you the property before they die. It could result in hefty taxes for them, diminishing any financial benefit to you.

#7. Consider Buying Whole Life Insurance

When it comes to life insurance, we often think about providing for our loved ones in the event of our passing. However, a clever strategy employed by wealthy people is purchasing whole life insurance. It serves as both an insurance policy and an investment account.

To enjoy the tax benefits, allow your policy to experience tax-deferred growth. Additionally, under specific conditions, you may receive tax-free distributions. The advantage here is that affluent policyholders benefit from these tax breaks during their lifetime. Upon their demise, the policy’s benefit amount goes directly to the chosen beneficiary, who receives it tax-free.

To explore this option, seek guidance from a qualified financial planner or insurance agent. It’s essential to consult with an expert to determine if whole life insurance aligns with your financial goals. Some experts caution against it, citing potential downsides like expensive fees.

#8. Buying a Second Home for Tax Benefits

Many Americans can’t pay cash for a second home, but having more than one residence can help reduce a wealthy person’s tax bill.

If you own a home and itemize your deductions on your tax return, you can often deduct property taxes and mortgage interest. There’s a limit of $10,000 ($5,000 for married taxpayers filing separately) for property tax deductions. If you purchase a second home, you can also deduct taxes and mortgage interest on that property.

The IRS says a second home can qualify as a home if it has sleeping quarters, a kitchen, and a toilet. While this might not be practical for those who can’t afford a second home, even if you own just one home, it’s worth exploring the tax breaks for homeowners.

#9. Open a Health Savings Account (HSA) for Tax Benefits

Consider opening a Health Savings Account (HSA) for potential triple tax benefits. Firstly, the money you put into an HSA is tax-deductible, even if you don’t itemize deductions. Secondly, any earnings in the account grow tax-free. Lastly, withdrawals are tax-free when used for qualifying healthcare expenses, subject to the same rules as deductible medical and dental expenses on Schedule A. Be cautious though, using the money for non-healthcare expenses may result in a 20% penalty.

For an added advantage, once you’re 65 or if you become disabled, you can withdraw HSA funds for any purpose without penalty. Just remember, if you spend the money on non-health expenses, you’ll still owe ordinary income federal taxes.

How to Claim the Deduction

To claim the HSA deduction, open an HSA and contribute to it. Not everyone is eligible, though. You must be part of a high-deductible medical insurance plan that is HSA-eligible. In 2024, contribution limits are $4,150 for individuals and $8,300 for families. Use Form 8889 to report contributions, calculate deductions, and manage HSA taxes and penalties.

#10. Open a Solo 401(k) Plan

If you work for a big company, you’ve probably heard about the 401(k) plan. It lets you put money in and grow it without paying taxes until later. Now, if you’re self-employed, don’t feel left out.

You can also open your own solo 401(k) plan. And guess what? You can put in a whopping $66,000 for 2023 and $69,000 for 2024. That’s way more than what folks in regular 401(k)s can do. And if you’re 50 or older, you can add another $7,500.

To claim this deduction, first things first, set up your solo 401(k) plan at a bank or brokerage account. Then, when tax time rolls around, fill out IRS Form 5500 to tell them about the money you put in.

#11. Delay Your Income for Deferred Tax Benefits

Delaying income can be a smart tax strategy. You only pay taxes on the income you receive in a year. If you finish a job and are owed payment but delay receiving it until the next year, you won’t owe taxes on it until then. So, by pushing back the receipt of income by even a day, like from December 31 to January 1, you get an extra year before you have to pay taxes on it.

To put it simply, when you defer income to a future year, you just leave it out of your tax filing for the current year. For instance, if you’re expecting a bonus on December 31 but ask your employer to pay it on January 1, you include that income on your tax return for the following year. It’s that straightforward.

#12. Harvest Tax Losses to Save on Taxes

In the U.S., if you make profits in taxable accounts, you have to pay capital gains tax. If those gains are short-term (held for a year or less), you could end up paying a hefty 37% in federal tax, especially if you’re in the top tax bracket.

A smart move to avoid high short-term gains tax is to use a strategy called “harvesting losses.”

If any of your investments are trading at a loss, sell them to realize those losses. You can then use these losses to offset your capital gains. If your losses are more than your gains, you can even deduct up to $3,000 from your ordinary income, which means more tax savings.

So, a loss on paper can turn into significant tax savings if you use it to balance out your gains. Just remember to report your capital transactions on Form 8949 and summarize the gains and losses on Schedule D.

Are there ways to make rich people pay more taxes?

Getting wealthy individuals to pay more taxes is a challenge due to the legal methods they employ to avoid taxation. Despite President Biden’s initial proposal for a national wealth tax, progress has stalled. Some states like California, Connecticut, Hawaii, Illinois, Maryland, Minnesota, New York, and Washington are taking matters into their own hands by suggesting plans to tax the rich. Each state has its unique approach, often involving taxing assets and reducing the threshold for estate taxes.

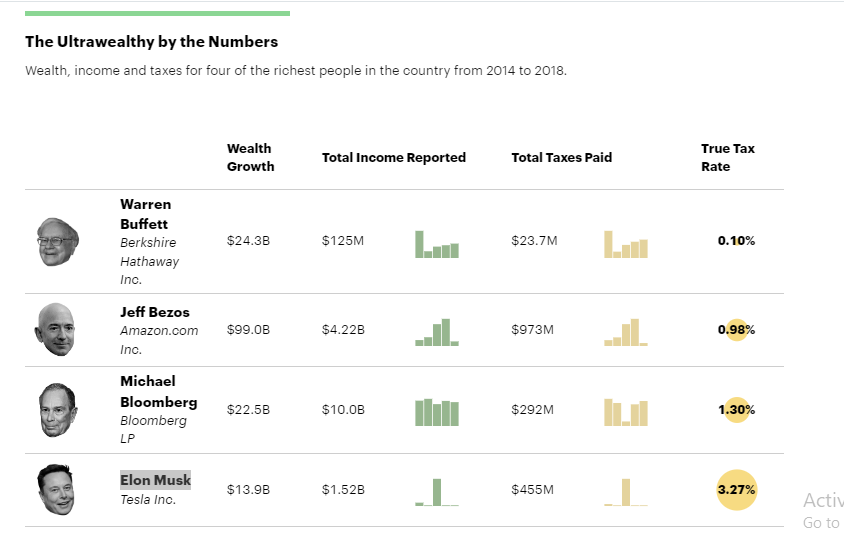

Uncovering the True Tax Rates of America’s Wealthiest

Are America’s billionaires using tax avoidance strategies that regular folks can’t access? Yes. Their wealth comes from the booming value of assets like stocks and property, which aren’t considered taxable income unless they’re sold.

To reveal the financial reality of the richest Americans, ProPublica did something unprecedented. They compared the taxes paid by the 25 wealthiest Americans each year to the growth in their wealth estimated by Forbes during the same period.

So, what did their survey find? From 2014 to 2018, these 25 individuals saw their combined wealth shoot up by a staggering $401 billion. Surprisingly, they only paid a total of $13.6 billion in federal income taxes during that time, according to IRS data. This amounts to a true tax rate of just 3.4%.

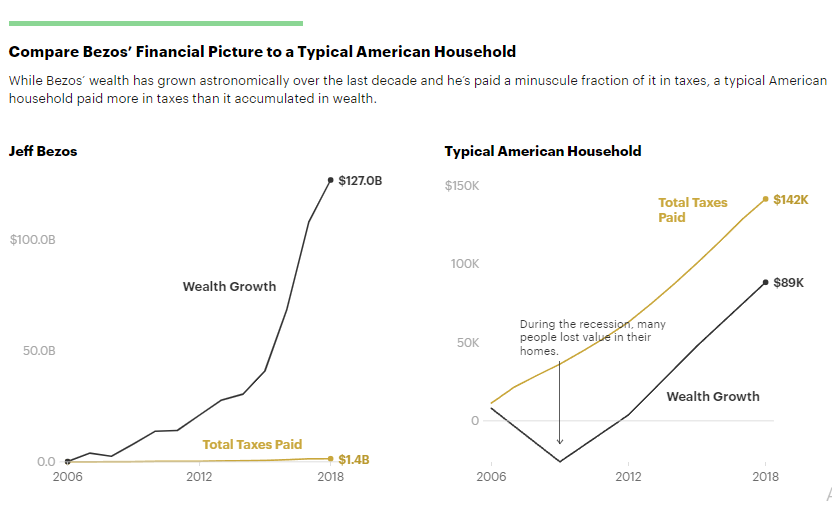

Now, let’s contrast this with middle-class Americans – say, wage earners in their early 40s with an average amount of wealth for their age group. From 2014 to 2018, their net worth increased by around $65,000 after taxes, mainly because of the uptick in their home values. However, due to the majority of their earnings being salaries, their tax bills were nearly as much – nearly $62,000 – over those five years.

In essence, this sheds light on a stark contrast in how taxes are playing out for the super-rich versus the middle-class

Case Study –

Let’s take Jeff Bezos’ tax situation in 2007. Despite his wealth skyrocketing by $3.8 billion, he paid zero federal income taxes. How? Bezos, filing jointly with his then-wife, reported only $46 million in income, mostly from interest and dividends. He offset every penny with losses from investments and various deductions, such as interest expenses and “other expenses.”

In 2011, with his wealth at $18 billion, Bezos claimed a loss on his tax return, as income was outweighed by investment losses. Remarkably, he even got a $4,000 tax credit for his children because, according to the tax law, he made so little.

Examining 2006 to 2018, when Bezos’ wealth surged by $127 billion, he reported a mere $6.5 billion in income. Despite paying $1.4 billion in personal federal taxes, it translates to just a 1.1% true tax rate on the increase in his fortune. The details expose a significant aspect of how the wealthy navigate the tax landscape in the United States

Bottom Line –

Make sure to pay what you legally owe in taxes, but there’s no need to pay extra. Spend a few hours on the IRS website and reputable financial sites to find potential tax savings worth hundreds or even thousands of dollars.

Before claiming these savings on your tax return, it’s smart to check with a tax professional. Make sure you qualify when all the intricate rules are applied, and then enjoy the money you saved due to your diligence.

Editor’s Choices:

1040 Tax Form Evolution: Everything You Need To Know For Tax Planning In 2024

Tax Planning 2024: When, How And Where To Start Filing Your Taxes

Gambling Winnings And Tax Strategies: Smart Planning For Unexpected Fortunes