Are you a parent who loans money to your kids for things like a bike, their first car, or even a home? Wondering if the IRS cares about it?

Good news: Small loans to your children don’t bother the IRS. But if it’s a significant amount, charging some interest can help you avoid gift tax issues. And if your child can’t pay it back, there’s something called a bad debt deduction.

In today’s blog, we’ll dive into all these aspects and break things down for you.”

Understanding Family Loans

Family loans are simply loans between family members or close friends. They’re informal, with no fancy paperwork, credit checks, or formal applications. These loans might be sealed with a handshake or a written agreement, which is a better idea (we’ll explain why soon).

Family loans can range from big to small, helping with various needs. For example, an uncle might lend $50,000 to his niece for a home down payment, or a mom could give $3,000 to her son during a rough patch.

These loans come with advantages:

- No need for complicated applications or credit checks.

- Interest rates are usually lower than what banks offer.

- They keep your family away from high-interest loans like payday loans.

However, there are downsides too:

- Awkward situations can arise if the borrower struggles to repay.

- These loans won’t boost the borrower’s credit score since credit bureaus don’t track them.

- Tax matters can pop up (we’ll delve into this shortly).

It’s vital to weigh the cons, especially the potential for family tension if things go south.

Discuss your concerns before diving into a family loan.

Now, let’s talk taxes, which depend on the loan’s size. Smaller loans under $10,000 are usually informal and don’t get tangled in complex interest rate rules (we’ll clarify this soon). But if you’re dealing with a loan over $10,000, IRS rules come into play.

Are Family Loans Taxed?

Yes, family loans can have tax implications for both the lender and the borrower. It depends on how you structure the loan and its size.

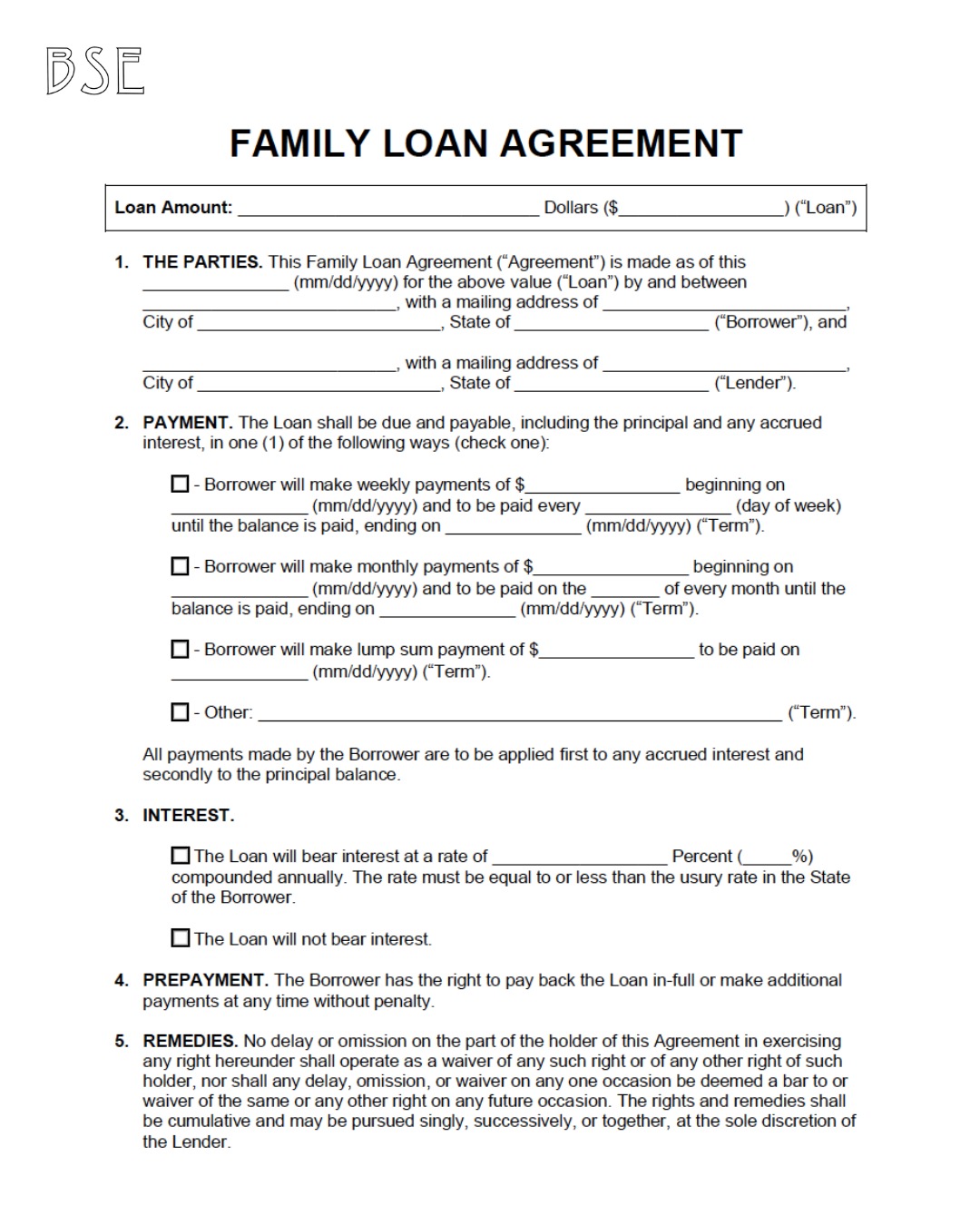

- Use a Loan Agreement: Always create an official contract signed by both parties. The IRS requires this to distinguish loans from gifts. Without it, the IRS might consider it a gift subject to gift tax rules.

- Charge Some Interest: The IRS prefers family loans to have interest. Interest-free loans have complex tax rules. The interest payments could be subject to income tax, not the loan itself. So, if you lend $50,000, you won’t pay tax on the loan amount, but you may need to pay income tax on the interest you receive.

- Avoid Messy Situations: If you don’t charge interest, you might have to pay tax on the interest you could have charged, which can be messy. It’s simpler to charge a modest amount of interest.

- Smaller Loans Are Easier: Loans under $10,000 are usually not subject to minimum interest rules, making them easier to handle without much tax hassle.

Does the IRS Care If I Lend Money to My Kids?

For small loans under $10,000, no need to worry – the IRS doesn’t care. They’re fine with personal loans to your kids or immediate family, regardless of interest or repayment frequency.

But, there are exceptions when lending larger sums.

Interest-Free Loans

If you lend over $10,000, it’s a good idea to charge interest. Otherwise, the IRS might see the unpaid interest as a gift. This can count towards your annual gift limit of $17,000 per individual (as of 2023). Giving more requires filing a gift tax form.

The interest rate should be based on IRS-set applicable federal rates (AFRs) or the borrower’s net investment income for the year. You can skip interest if the borrower’s investment income is $1,000 or less. Charging interest below the AFR is called a below-market loan, which has tax implications. Check the article’s last section for more on this and some exceptions.

Is lending money to your kids the same as giving them gifts?

The IRS doesn’t buy it if you try to give a big chunk of cash to your children and label it as a loan to dodge gift tax rules. To avoid this, your loan must be legit and legally binding, or it might be considered a gift.

When you’re lending money to a family member, it’s a smart move to consult with a legal expert and create a formal loan agreement for both parties to sign.

What about student loans for education?

You can offer “student loans” to support your child’s education by setting up an official loan contract, just like any other loan. After they graduate and start repaying, your kids can claim a student loan interest deduction on the interest they pay to you. But remember, you’ll have to pay taxes on that interest income to the IRS.

What if your child doesn’t repay the loan?

One perk of having a loan agreement is that if your child can’t repay it, you can take a deduction for a non-business bad debt. Plus, you won’t have to worry about gift tax payments to the IRS as you would if you had given the money outright.

To claim a bad debt deduction, you must demonstrate that the debt is genuinely uncollectible. Have your child provide a written statement confirming they can’t repay, and gather evidence that you’ve made efforts to collect the debt, such as letters, invoices, and phone call records. This evidence will back up your case with the IRS.

Filing a gift tax return for a loan

But what if you don’t properly document the loan, and the IRS thinks it’s a gift?

In most cases, you won’t owe taxes for a “loan” that the IRS considers a gift. Even if you go over the $17,000 yearly gift limit we mentioned earlier, you only pay gift tax when your lifetime gifts to everyone exceed $12.92 million for 2023 (it was $12.06 million in 2022).

You’re probably safe, but keep track of and report any gifts above $17,000 in 2023.

Other family loans that are safe from tax consequences No need to worry about tax consequences for family loans if:

You lend a child $10,000 or less, and they don’t invest it in things like stocks or bonds.

You lend a child $100,000 or less, and their investment income is under $1,000 for the year.

If you don’t fit into these exceptions, check out IRS Publication 550 for info on below-market loans and their tax implications.

Bottom Line

To keep things straightforward, create a written agreement with clear terms and charge a small interest based on federal rates.

This way, you’ll have to report and pay income tax on the interest, but it’s a better choice than the complications of interest-free loans.

For more on personal finance and giving money to your family, explore the BSE Accounting blog for helpful tips and insights.

Editor’s Choice:

How The Rich Avoid Paying Federal Taxes (And How You Can Too)

Tax Form 1040 Evolution: Everything You Need To Know For Tax Planning In 2024

Tax Planning 2024: When, How And Where To Start Filing Your Taxes

Gambling Winnings And Tax Strategies: Smart Planning For Unexpected Fortunes

The No-Go Zone: A Roadmap For Non-Tax Deductible Business Expenses

Get Your Business Back On Track: Dealing With IRS Back Taxes