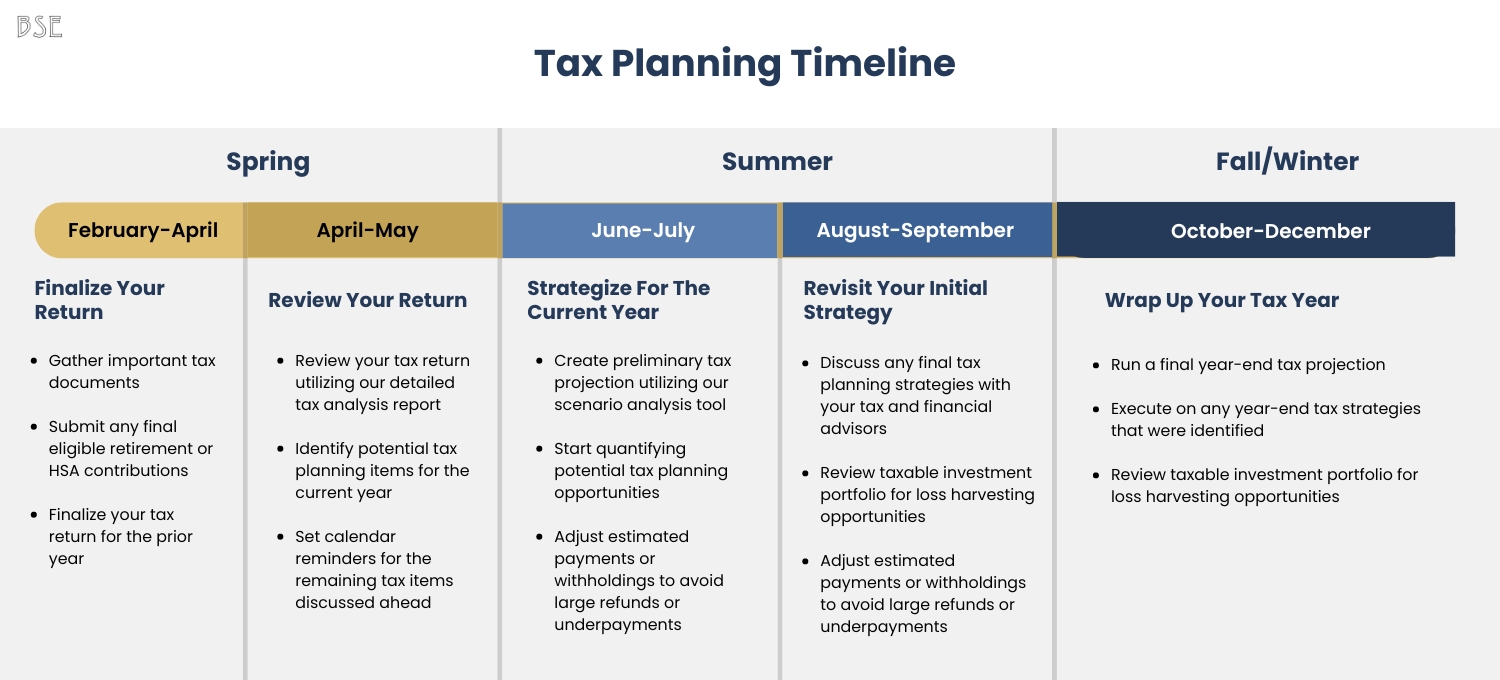

As the year-end approaches, I know how stressful it can be to juggle tax planning with everything else on your plate. It’s easy to feel overwhelmed and risk overpaying on your taxes, especially with ever-changing rules and deadlines. That’s why I’m here to help you cut through the clutter.

In this blog, I’ll walk you through proven strategies to slash your tax bill and maximise your refund before the year wraps up. We’ll dive into crucial areas like savvy deductions, smart moves for your stock portfolio, and leveraging safe harbour tax laws.

I’ll also cover last-minute medical plan strategies, retirement deductions, the ins and outs of Roth IRAs and a lot more. With these insights, you’ll not only navigate the tax season with confidence but also come out ahead. So, let’s get started and make sure you’re not leaving money on the table.

Last-Minute Year-End General Business Income Tax Deductions for 2024

The IRS may not hand you a check for the money they owe, but with the right strategies, you can reduce your tax liability. These six powerful business tax deduction strategies for 2024 will ensure you pay less in taxes, saving more for your business. Implement them before the end of the year to make the most of your deductions.

1. Prepay Expenses Using the IRS Safe Harbor

One of the most underused yet effective year-end tax-saving strategies is prepaying expenses. The IRS offer a key tax planning strategy for cash-basis taxpayers, known as the “Safe Harbor Rule.” This allows businesses to prepay qualifying expenses and deduct them up to 12 months in advance without triggering any IRS adjustments or challenges. The strategy becomes highly effective when used for year-end deductions, giving businesses a legitimate way to lower their tax liability before the year closes.

But You might be wondering how it works?

So, under this safe harbour, businesses can prepay expenses like rent, insurance, and leasing payments for business vehicles or equipment.

The key rule is that the prepayment cannot cover more than 12 months of expenses, and the prepayment cannot extend beyond the following tax year. This ensures that the IRS doesn’t flag it as an attempt to improperly defer income.

For example, a business can prepay rent for the entirety of 2025 before December 31, 2024, and deduct that expense in their 2024 taxes. However, if they attempt to prepay rent for 2026 or beyond, they would be crossing the 12-month safe harbor limit, and the IRS could disallow the deduction.

Qualifying Expenses: Some of the qualifying expenses for prepayment under the IRS guidelines include:

- Rent on offices, warehouses, or machinery

- Business insurance premiums (such as liability or malpractice insurance)

- Lease payments for business vehicles or equipment

By leveraging these prepayments, businesses can reduce taxable income in the current year while managing cash flow effectively.

How to Leverage the Safe Harbor Rule?

Let’s say you own a small business and are on a cash basis for tax purposes. You rent office space and currently pay $5,000 per month in rent. Knowing that your business will have higher income in 2024 and you want to lower your tax burden, you decide to prepay your office rent for 2025 before the year ends.

- On December 27, 2024, you write and mail a check to your landlord for $60,000, covering all rent payments for 2025.

- Your landlord receives the check in January 2025 and records the income for the 2025 tax year.

and the result ….

- You get to deduct the full $60,000 in 2024, lowering your taxable income for that year.

- Your landlord doesn’t have to recognize the $60,000 as income until 2025, which aligns with their financial planning.

This strategy works perfectly for you because you reduce your taxable income by $60,000, potentially moving you into a lower tax bracket for 2024.

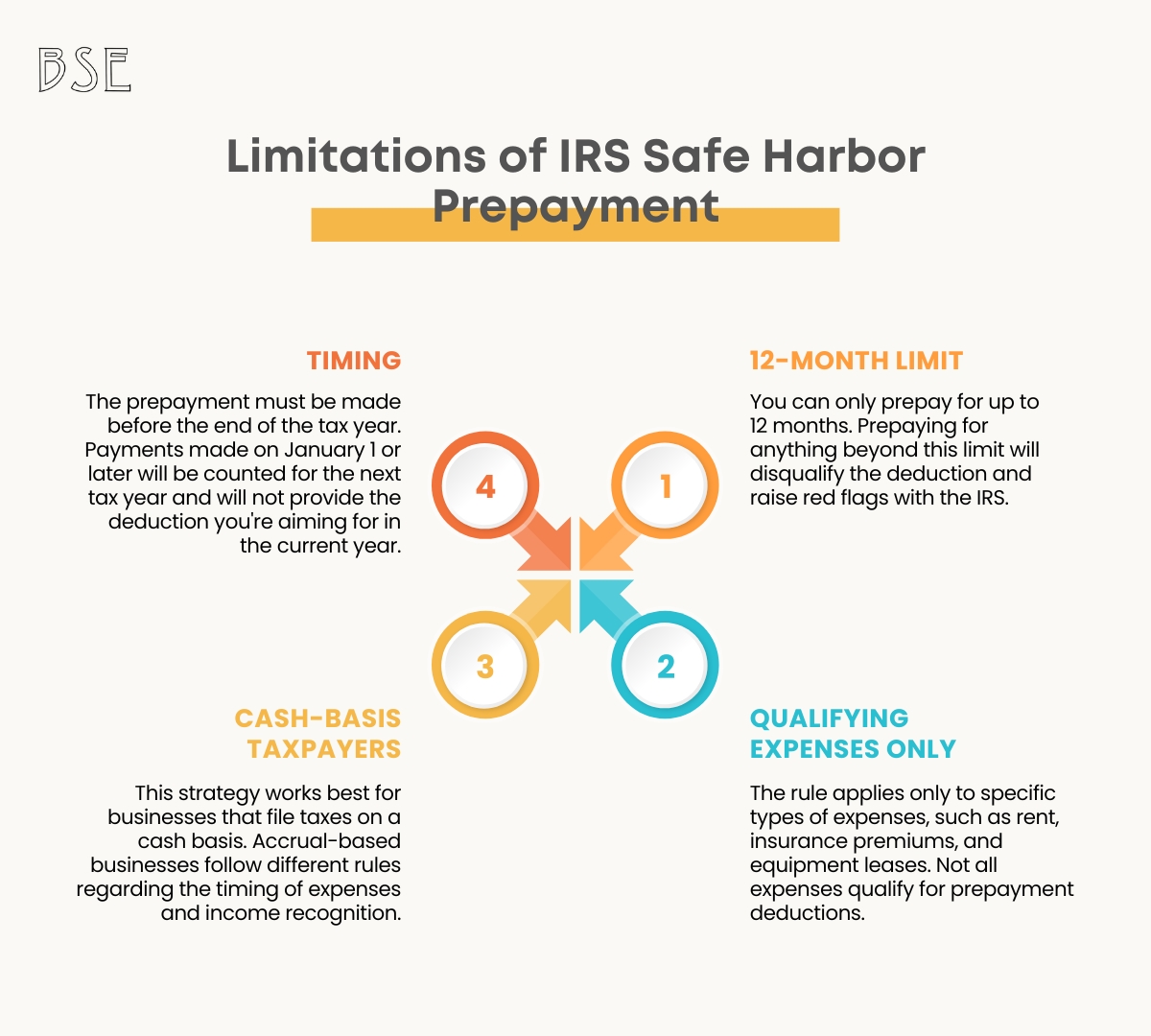

Limitations of IRS Safe Harbor Prepayment

While the Safe Harbor Rule is an excellent tool for reducing taxable income, there are some limitations businesses should be aware of:

- 12-Month Limit: You can only prepay for up to 12 months. Prepaying for anything beyond this limit will disqualify the deduction and raise red flags with the IRS.

- Qualifying Expenses Only: The rule applies only to specific types of expenses, such as rent, insurance premiums, and equipment leases. Not all expenses qualify for prepayment deductions.

- Cash-Basis Taxpayers: This strategy works best for businesses that file taxes on a cash basis. Accrual-based businesses follow different rules regarding the timing of expenses and income recognition.

- Timing: The prepayment must be made before the end of the tax year. Payments made on January 1 or later will be counted for the next tax year and will not provide the deduction you’re aiming for in the current year.

Let’s understand this more with an example:

Imagine you’re a business owner who wants to prepay rent for both 2025 and 2026 to maximize your deductions for 2024. You decide to write a check for $120,000 to cover two years of rent payments. While you may think this will reduce your 2024 taxable income significantly, you’re only allowed to deduct $60,000—the amount that covers 12 months of rent. The extra $60,000 won’t qualify for a deduction in 2024 and could raise IRS scrutiny..

For more on this, refer to the IRS Prepayment Guidelines.

2. Stop Billing Customers, Clients, and Patients Until 2025

When it comes to reducing your taxable income, understanding IRS Cash Basis accounting is crucial for business owners, freelancers, and entrepreneurs. Under the cash basis method, you report income in the year you receive it and deduct expenses in the year you pay them.

Like, if your business operates on a cash basis, consider delaying billing until after December 31, 2024. This strategy is simple but highly effective in postponing income and reducing your current year’s taxable income.

When you delay sending invoices, customers won’t pay until they’re billed, meaning the income won’t be recognized until the following year.

How Does IRS Cash Basis Work?

- Income Reporting: You record income only when cash or payments are actually received.

- Expense Deductions: You deduct expenses when they are paid, not when incurred.

This gives you flexibility because you can delay income by postponing billing or accelerate deductions by prepaying expenses, as discussed in the strategies earlier. Businesses on a cash basis find that they can better manage their taxable income by controlling when they recognize income and expenses.

For Example –

Let’s say you’re a freelance graphic designer operating under the cash-based method, and it’s December 2024. You’re looking to reduce your taxable income for the year.

Here’s how you could use the cash basis to your advantage:

- Delay Income: You usually bill your clients at the end of every month. To avoid having to report additional income in 2024, you could delay billing clients until January 2025. This postpones the recognition of income, effectively pushing it into the next tax year.

- Accelerate Expenses: You have $10,000 worth of office rent for 2025. By prepaying in December 2024, you can deduct the expense this year, reducing your taxable income for 2024.

If your gross income is $90,000, the $10,000 rent prepayment could reduce your taxable income to $80,000, saving you thousands in taxes.

But… pay attention !!!!!!

While cash basis accounting offers significant tax-saving opportunities, it does have some limitations:

- Inaccurate Financial Picture: The cash basis method doesn’t always give an accurate picture of your business’s financial health since it only accounts for cash transactions. For instance, if you’ve earned income but haven’t received payment, it won’t show up as income until cash is in hand, potentially underreporting your earnings.

- Not Suitable for Large Businesses: The IRS restricts cash-based accounting for businesses with gross receipts over $27 million (as of 2024). Businesses that exceed this limit must use the accrual method.

- Limited to Certain Types of Expenses: Some expenses, like capital expenditures (e.g., buying machinery or property), can’t be deducted immediately under the cash basis method and require depreciation over time.

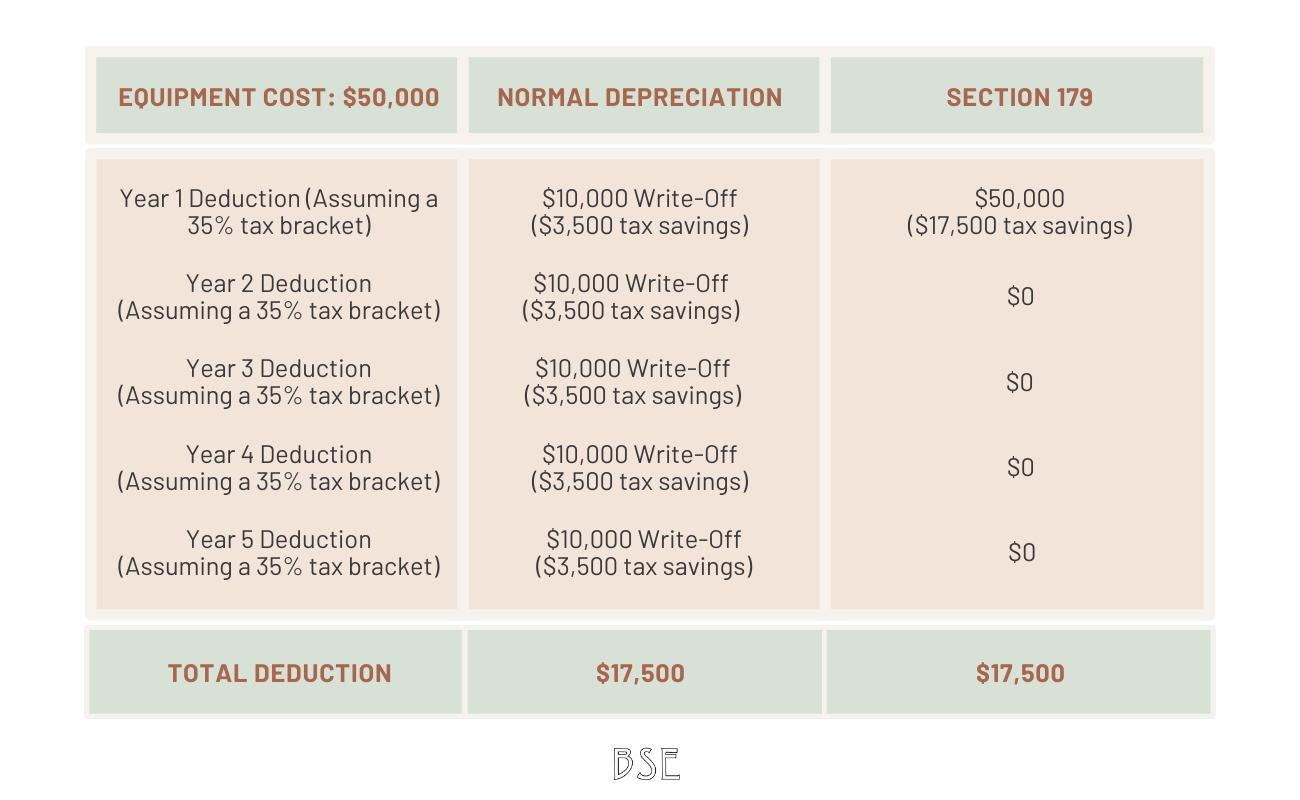

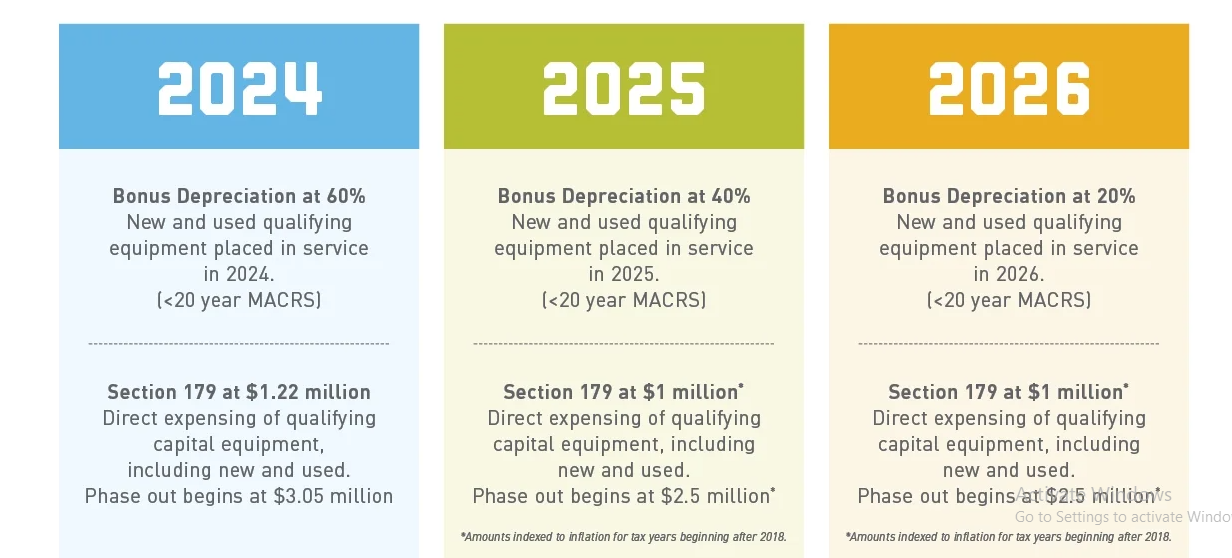

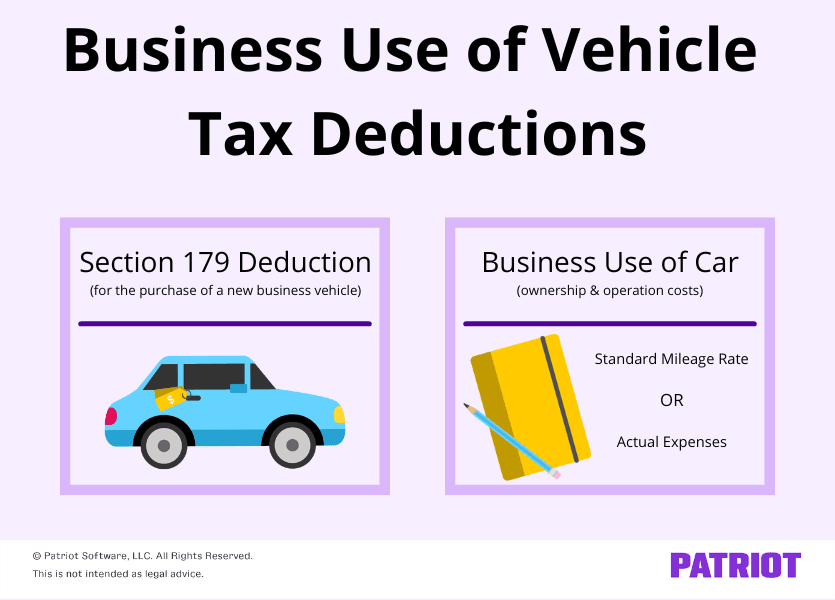

3. Invest in Office Equipment and Get Section 179 Expensing

When it comes to tax savings, Section 179 and Bonus Depreciation are two powerhouse tools for business owners. If you’re thinking about investing in new or used equipment for your business, these provisions can give you a massive financial boost by allowing you to write off the full cost of qualifying purchases in the same year.

a. But what actually is Section 179?

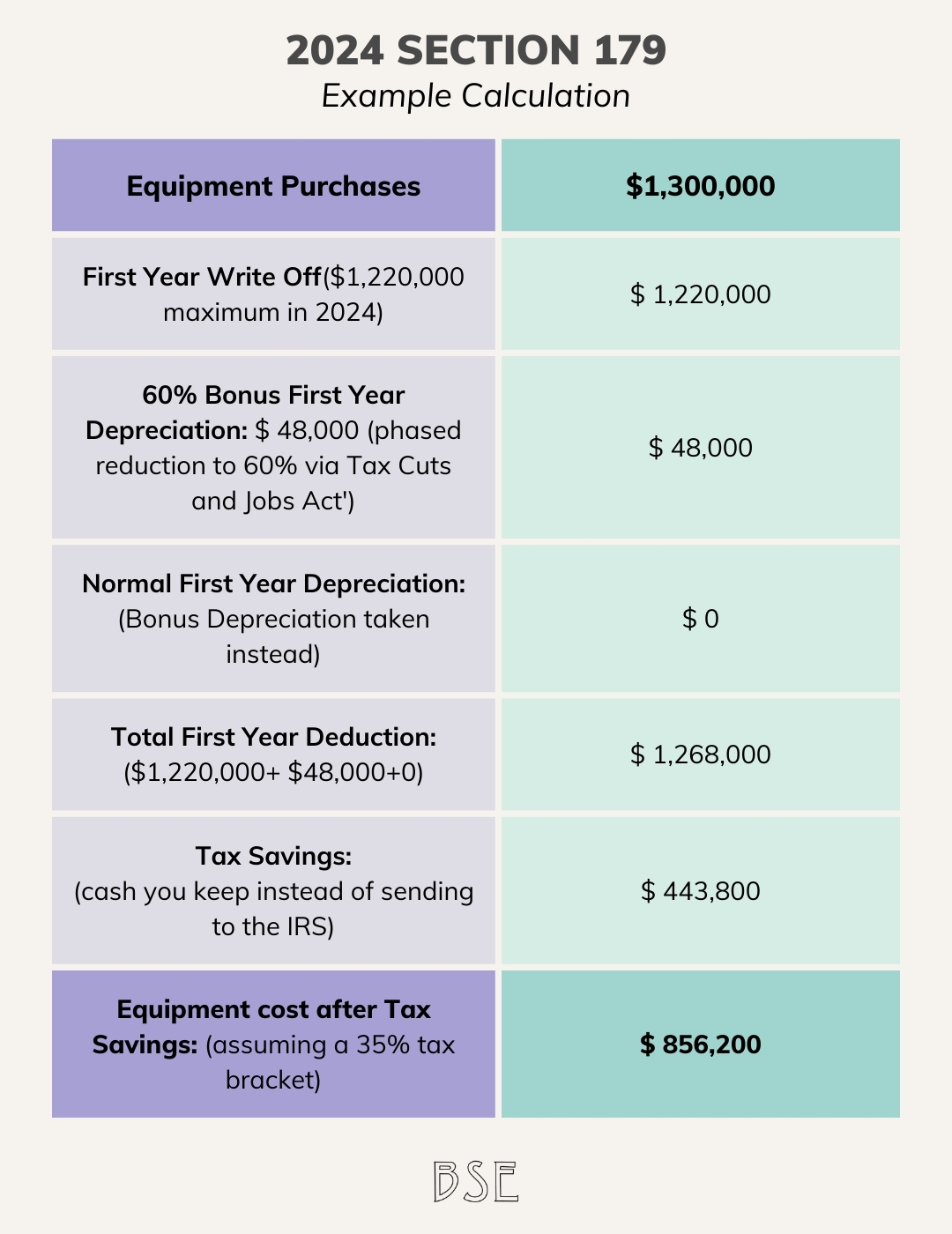

Section 179 lets businesses deduct the full cost of certain qualifying property—like equipment, furniture, and even certain vehicles—up to a limit. For 2024, the deduction limit is set at $1.16 million, which means that if your business buys a piece of equipment, you can write off the entire cost (up to that limit) instead of spreading the deduction out over several years.

The key is that the equipment must be purchased and put into use before the end of the tax year to qualify.

b. Bonus Depreciation – The Extra Punch

Bonus depreciation goes hand-in-hand with Section 179. After you’ve hit the Section 179 limit, bonus depreciation allows you to deduct 80% of the remaining cost of your purchases. Unlike Section 179, there’s no spending cap. So, if you’re making large purchases—like buying multiple pieces of equipment—bonus depreciation ensures that you’re still getting major tax savings even after you max out Section 179 deductions.

Here’s the catch with bonus depreciation: it’s set to phase out after 2026 unless Congress extends it.

For 2024, though, it still allows you to write off a huge chunk of your purchases, which makes it incredibly valuable if you’re investing heavily in your business this year.

c. How It Helps? Understand with an example

Let’s say you run a small manufacturing business and you buy $1 million worth of new equipment in 2024 to boost your operations. Thanks to Section 179, you can immediately deduct the full $1 million from your taxable income, giving you a huge tax break.

But what if you bought even more? Let’s say you invested $2 million. After you deduct $1.16 million using Section 179, you could use bonus depreciation to deduct 80% of the remaining $840,000. That’s an additional $672,000 deduction, bringing your total write-off for the year to $1.832 million.

Imagine how much that would save you in taxes.

Now let’s talk about some Limitations and Where It Can Fall Short

Section 179 and bonus depreciation sound like a dream come true—and they are, for the right businesses.

But there are limitations to be aware of:

- Profitable Businesses Only: You can only deduct up to the amount of your taxable income with Section 179. So, if your business isn’t making money, this deduction doesn’t help you. In that case, bonus depreciation might be a better option because it allows you to create a tax loss, which can be carried forward to future years.

- Property Use: Not all purchases qualify. Section 179 applies only to tangible property like machinery, equipment, and software. It doesn’t apply to land, buildings, or inventory. Bonus depreciation has a broader scope, but still has some limitations.

- Cap on Section 179: While the $1.16 million limit sounds generous, businesses with big purchases or high-income thresholds may hit the cap and need to rely on bonus depreciation. But remember, bonus depreciation is phasing out, so plan your purchases accordingly.

Using these strategies wisely can save your business significant money on taxes, but it’s important to assess what fits your specific situation. If you’re looking to grow or invest in your business, Section 179 and bonus depreciation are tools you don’t want to overlook.

For more information, check out the IRS’s detailed breakdown on Section 179 here.

4. Use Your Credit Cards for Last-Minute Purchases

Using your credit card for last-minute purchases is a smart way to maximize your business tax deductions before the year ends. The IRS gives sole proprietors and single-member LLCs, filing a Schedule C, a handy benefit here: You can claim a deduction the very moment you charge something to your business or personal credit card.

This means if you’re looking to stock up on office supplies, buy that new business laptop, or even cover travel expenses, you don’t have to wait until you actually pay the bill. As long as the charge hits your account by December 31, 2024, it counts as a deduction for this tax year, even if you don’t pay off the balance until 2025.

Why This Works Well for Sole Proprietors or LLCs

For someone filing a Schedule C, this immediate deduction can provide a quick and simple way to reduce taxable income. Instead of worrying about having enough cash on hand, you can simply charge it and still get the benefit. Plus, this can be a great way to take advantage of any rewards points or cashback programs your credit card offers, giving you an extra boost while also cutting down your tax bill.

Let’s say you’re running a freelance design business as a sole proprietor. You’ve been eyeing a new graphic design software package for $1,200 that’ll help you take on more clients.

You charge it to your credit card on December 30, 2024. Even though you won’t pay your credit card bill until January 2025, the IRS lets you deduct that $1,200 as an expense for the 2024 tax year. You get to reduce your taxable income right away, helping you keep more money in your pocket.

For example

Let’s imagine SAM, a single-member LLC that runs an online retail business. Her business made a profit of $85,000 this year, but she’s looking for ways to lower her tax burden. On December 28, she decides to buy $5,000 worth of new packaging equipment on her business credit card.

Even though she won’t pay off the card until next year, she can still deduct the $5,000 from her 2024 taxes. This drops her taxable income to $80,000, and she ends up saving hundreds of dollars in taxes by just using her card strategically.

Now here are some limitations of this amazing tax strategy you should keep in mind

However, there are some things to watch out for. If you’re running your business as a corporation and using your personal credit card, the situation changes. The corporation won’t get the deduction right away—it only counts when the corporation reimburses you for that expense.

So, if you want to claim the deduction for 2024, you need to make sure your corporation reimburses you before the year ends.

Another thing to consider is the potential interest on those credit card purchases. If you carry a balance and end up paying high interest rates, those tax savings could get cancelled out by the extra fees you’re racking up. So, while using credit cards for year-end purchases can be a great tax strategy, make sure you’re not taking on unnecessary debt that outweighs the benefits.

By using your credit cards smartly, you can get ahead of your taxes without even having to part with cash immediately. Just remember to play it right and be aware of the rules that apply to how your business is set up.

5. Don’t Be Afraid of Excess Deductions

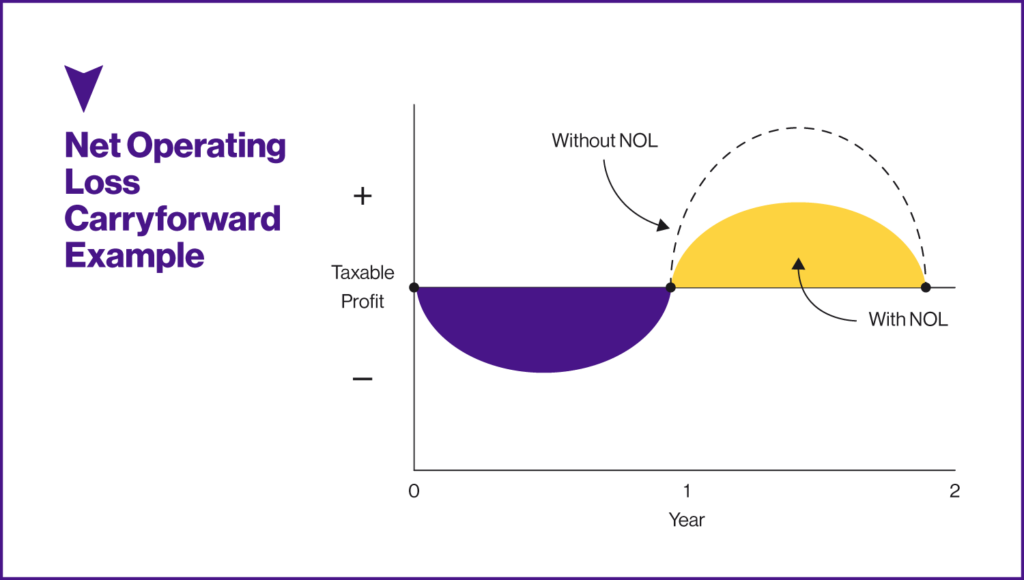

If your business deductions exceed your income for the year, don’t worry.Don’t hold back on claiming deductions just because you’re in a loss year. Every deduction counts. Claim every business expense you’re entitled to, even if it means creating a loss. That loss turns into your NOL, and that NOL will be a tax-saving powerhouse in the future. It can be carried forward to offset up to 80% of your future taxable income

Sure, it feels odd to be sitting on a loss, but in the grand scheme, it’s a strategy to slash your future tax bill. So, don’t leave any deductions on the table, especially if you’re in the early stages of your business, or experiencing a temporary dip in profits.

Now, you might think what are NOL Rules

So, When your business expenses outstrip your income, you’re in what’s called a Net Operating Loss (NOL) situation. Sounds like a bad thing, right? But for tax purposes, it’s actually a good deal.

Here’s why.

Before the Tax Cuts and Jobs Act (TCJA) of 2017, you could carry back an NOL for two years. That meant if you had a loss in 2024, you could apply it to your tax returns from 2022 or 2023, snagging yourself a nice refund from the IRS. That provision is now gone, but don’t worry—there’s still a huge advantage here. The TCJA lets you carry your NOL forward indefinitely.

In the short term, this won’t give you an immediate refund, but down the line, it can save you tons on future taxes. One thing to note, though: you can only use the NOL to offset up to 80% of your taxable income in any future year.

So How Does This Help You?

Let’s say your business had a rough year in 2024, and you’re looking at a $30,000 loss. While it stings in the moment, don’t forget about your trusty NOL. You can carry that $30,000 forward, and when your business starts booming in 2025 and you rake in $100,000, you can apply that NOL and only pay taxes on $70,000. Boom!!!!!!! That’s a huge win.

Now, there are some limitations. You can’t wipe out 100% of your taxable income using NOLs. As mentioned, it can only reduce up to 80% of your taxable income in a given year. So, if you have an NOL of $100,000 and make $50,000 in the next year, you’ll only be able to use $40,000 of that loss to offset your income, leaving you with $10,000 to still pay taxes on.

Also, you’ve got to stay diligent with your record-keeping. Make sure you’re documenting every expense so you can calculate that NOL properly and carry it forward.

6. Take Advantage of Qualified Improvement Property (QIP) Deductions

If you’ve made improvements to the interior of your business property, such as renovating your office or upgrading the space for employees, you may qualify for Qualified Improvement Property (QIP) deductions.

Qualified Improvement Property (QIP) is any improvement made to the interior of a building you own, provided the building is non-residential real property. This includes renovations, upgrades, or even installing new fixtures, as long as the improvements were placed in service after the building was originally put into use.

Why QIP Deductions are a Game Changer

Here’s why QIP deductions are a big deal:

- Accelerated Depreciation: Unlike standard property depreciation which takes 39 years, QIP is depreciated over just 15 years. This faster depreciation means you get to write off your improvements much sooner.

- Immediate Deductions: With Section 179 expensing, you can deduct the entire cost of your QIP in the year it’s placed in service. For 2024, you can also take advantage of 80% bonus depreciation. This means if you make improvements to your property this year, you could potentially deduct 80% of those costs right away.

Example: Suppose you spend $100,000 on upgrading your office space in 2024. Under the QIP rules, you could deduct $80,000 of that amount immediately using bonus depreciation, and the remaining $20,000 could be deducted over 15 years. This can lead to a substantial tax break in the year you make the improvements.

How QIP Helps Save Big on Taxes

By taking advantage of QIP deductions, you’re not only improving your property but also giving your tax bill a serious reduction. Here’s how:

- Huge Immediate Tax Savings: The ability to deduct the cost of improvements quickly can significantly lower your taxable income for the year. This is particularly valuable if you’re looking to offset income and reduce your tax liability.

- Future Savings: Even though you’ll be writing off a large portion of your improvements now, the benefits can continue. The remaining amount depreciated over 15 years means ongoing deductions in future years, spreading out your tax savings.

Some other points to consider as well:

While QIP deductions offer great benefits, there are some limitations and considerations:

- Timing Matters: To get the QIP deduction for 2024, the improvements must be placed in service by December 31, 2024. If you miss this deadline, you’ll have to wait until next year, which might not be ideal for your current tax planning.

- Specifics of the Property: QIP only applies to improvements on non-residential real property. Residential properties, or improvements made before the building was put into use, don’t qualify.

- Bonus Depreciation Limitations: The bonus depreciation rate of 80% for 2024 is set to decrease in the coming years. It’s crucial to act now if you want to maximize your deductions before the bonus rate drops.

Therefore, if you’re eyeing that office renovation or planning significant upgrades, consider using QIP deductions to boost your tax savings. Remember, timing and details matter, so keep an eye on the deadlines and specific requirements to make the most of this opportunity.

For more on QIP and how it fits into your tax planning, check out the IRS QIP Guidelines.

Last-Minute Year-End Tax Strategies for Your Stock Portfolio in 2024-25

As we head toward the end of the year, it’s time to take a close look at your stock portfolio and uncover hidden opportunities to reduce your 2024 income taxes. The tax code is full of ways to offset gains and reduce what you owe—if you know how to play by the rules. The goal? Turn your portfolio into a tax-saving gold mine. Let’s explore some powerful strategies to help you cut down your tax bill and maximize your wealth as the year wraps up.

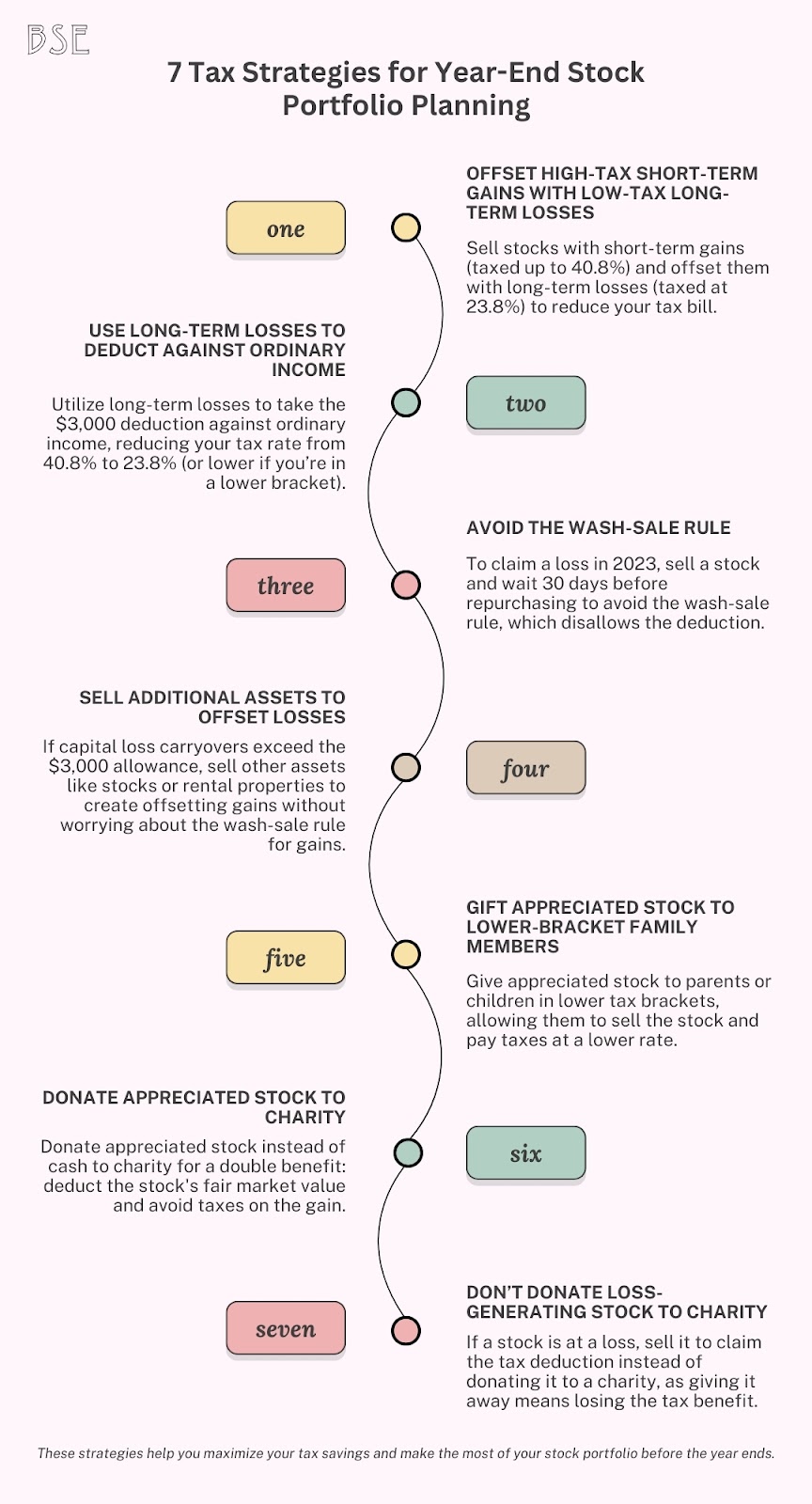

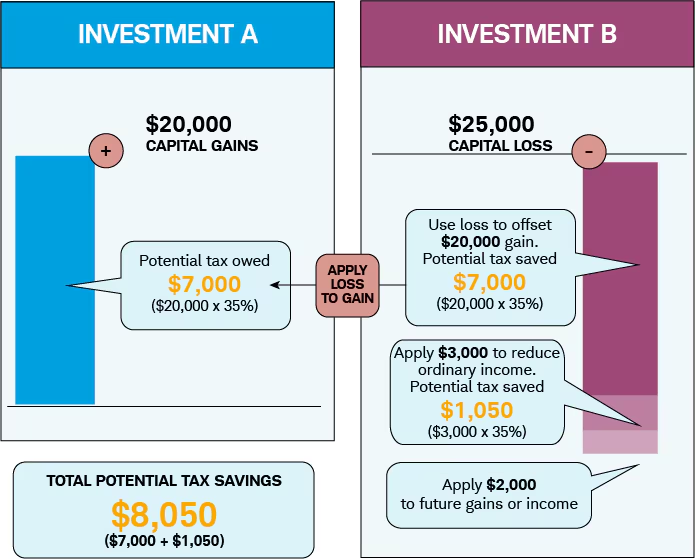

#Strategy 1. Offset Short-Term Gains with Long-Term Losses

When it comes to minimizing your tax bill, the strategy of offsetting short-term gains with long-term losses is one of the best tricks in the book. It’s simple yet powerful. Let’s break it down and look at how this strategy works, its benefits, a real-world example, and a few things you need to watch out for.

Why Offset Short-Term Gains?

First, let’s talk about short-term capital gains. These are the profits you make from selling assets you’ve held for less than a year. The IRS taxes these gains at your ordinary income tax rate, which can be as high as 40.8% (including the net investment income tax). That’s no small chunk of change, especially if you’re already in a high tax bracket.

On the flip side, long-term capital gains—profits from selling assets you’ve held for more than a year—are taxed at much lower rates, maxing out at 23.8%. This gap between short- and long-term tax rates is where the magic happens.

By selling investments at a long-term loss, you can use that loss to cancel out your short-term gains. In simple terms, you’re replacing a high-tax liability with a lower-tax cost, and that’s how you keep more of your money.

How Does It Work? Let’s Look at an Example

Say you had a great year and made a $10,000 profit by selling a stock you held for 10 months. That’s a short-term gain, which means it’s subject to the 40.8% tax rate. Without any strategies in place, you’re looking at paying $4,080 in taxes on that one trade alone.

But wait—now let’s say you also have another stock in your portfolio that you bought two years ago, and it’s currently down $10,000. By selling that stock and realizing the loss, you can offset your $10,000 short-term gain entirely. This way, you pay $0 in taxes on that profit. Instead of handing over nearly half your profit to the IRS, you get to keep it all.

That’s how you play the tax code’s offset game. You use your long-term losses to erase high-tax short-term gains.

Key Benefits of This Strategy

- Immediate Tax Savings: By offsetting short-term gains, you can avoid paying those hefty tax rates that can go as high as 40.8%.

- Improved Cash Flow: The less you owe in taxes, the more cash you keep in your pocket. This extra liquidity can be reinvested into new opportunities or just give you some breathing room for expenses.

- Long-Term Wealth Building: By keeping more of your gains, you can reinvest them and grow your portfolio faster over time.

But What Are the Limitations?

Like most strategies, offsetting short-term gains with long-term losses isn’t without its limitations. One downside to this approach is that you need to have losses in your portfolio to make it work. If you’ve only got winners and no underperforming stocks, you can’t offset anything. This strategy also requires a level of portfolio management and timing—selling stocks for a loss isn’t always easy or what you want to do.

Here’s another potential pitfall: if your long-term losses exceed your short-term gains, those excess losses can only offset up to $3,000 of your ordinary income per year. Any leftover losses will have to be carried forward into future tax years. This means you won’t get all your tax savings right away if your losses are larger than your gains.

#Strategy 2. Claim the $3,000 Loss Deduction Against Ordinary Income

One of the best-kept secrets in tax planning is that you can use capital losses to offset ordinary income—and this can be a real lifesaver when it comes to cutting down your tax bill. The IRS allows you to deduct up to $3,000 in net capital losses each year against ordinary income, and if you’re married and filing separately, the limit is $1,500.

Now, this may not seem like a huge number, but it can have a big impact, especially if you’re in a higher tax bracket. Let’s break it down so you can see just how much of a difference this deduction can make in real-life terms.

The Power of $3,000 in Tax Savings

Let’s say you had a tough year in the market and ended up with $10,000 in long-term capital losses. While those losses can offset your gains dollar-for-dollar, any leftover losses can also be used to reduce your ordinary income. The IRS allows you to knock $3,000 off your ordinary income for the year.

Here’s why this matters: If you’re in the 40.8% tax bracket, deducting $3,000 from your ordinary income translates to a tax savings of $1,224. That’s like finding money in your couch cushions, but better, because it directly reduces what you owe.

Even if you’re in a lower tax bracket, the benefit is still significant. For example, if you’re in the 24% tax bracket, your tax savings from the same $3,000 deduction would be $720. This is especially handy when you’re looking for ways to trim down your tax bill without much effort.

Example: How It Works

Let’s look at a real-world example to see this in action. Say you’re an investor who made $2,000 in short-term gains this year but also took a loss on another investment, losing $5,000. After you’ve used $2,000 of your losses to offset your gains, you’re left with $3,000 in net losses.

Thanks to the IRS rules, you can apply those $3,000 in losses directly to your ordinary income. If you’re earning $100,000 this year and in the 40.8% tax bracket, the $3,000 deduction brings your taxable income down to $97,000, saving you $1,224 in taxes.

Carrying Over Losses

What happens if your losses exceed the $3,000 limit? Don’t worry—you don’t lose them. Any leftover losses can be carried forward to future years. For instance, if you had $7,000 in losses, you’d deduct $3,000 this year and carry over the remaining $4,000 to next year. This means you can keep chipping away at your tax bill year after year, which is a nice bonus for long-term tax planning.

Limitations and Considerations

Now, there’s one downside to this strategy: it’s capped at $3,000 per year. So, if you have a large amount of capital losses, like $20,000, the immediate impact on your ordinary income is limited. You’ll only be able to deduct $3,000 this year, with the rest carried over.

For investors with significant losses, this can feel like a slow payoff, especially if you’re eager to see a big reduction in your taxes right away. But the upside is that, over time, those losses can still be used to lower your tax bill in future years. So, while it may not all happen at once, it’s still a valuable tool for long-term tax reduction.

Why It’s Worth It

Even though the limit is $3,000, it’s still worth using every penny of it. Think of it as easy money—whether it’s knocking down your tax bill by hundreds or thousands, it’s still better than paying full price to Uncle Sam. And if you’re in a high tax bracket, this deduction becomes even more valuable.

It’s also a great way to reduce your taxable income in a high-income year. If you had an especially good year for bonuses, salary, or other taxable income, using capital losses to take the edge off can soften the tax blow and keep more of your earnings in your pocket.

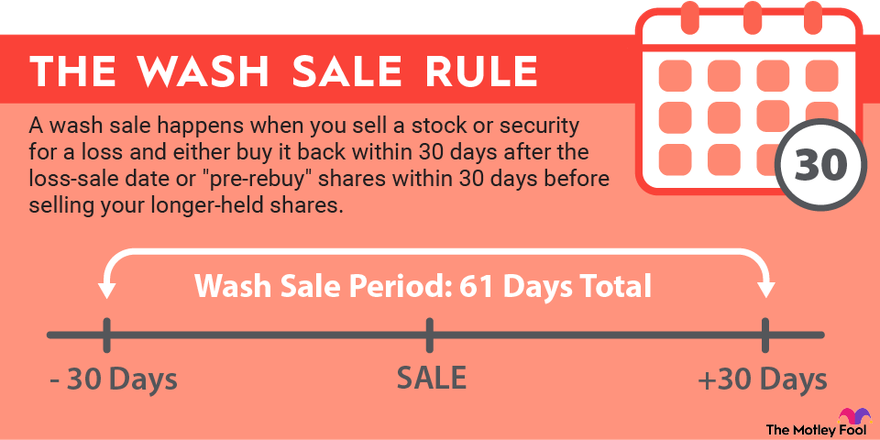

#Strategy 3. Avoid the Wash-Sale Rule

The wash-sale rule can be a bit of a hidden trap for investors. It stops you from claiming a loss on a stock sale if you repurchase the same or a “substantially identical” stock within 30 days. So, if you’re hoping to lock in a tax-deductible loss in 2024, you’ll need to play it smart to avoid this rule.

Let’s break it down: If you sell a stock and then quickly buy it back (either before or after the sale, within that 30-day window), the IRS says, “Nope, not so fast!” They won’t let you deduct the loss on your taxes. Instead, they make you add the loss to the cost basis of the new stock, meaning you’ll have to wait even longer to benefit from that loss.

But here’s the good news: You can easily sidestep this rule, and doing so can really boost your tax-saving potential.

The Benefits of Avoiding the Wash-Sale Rule

Why should you care about the wash-sale rule? Well, avoiding it means you can lock in your losses and immediately use them to reduce your taxable gains or even deduct from your ordinary income.

Here’s an example to make this clearer. Let’s say you’ve got a stock that has lost value—maybe you bought it for $10,000, and now it’s only worth $7,000. You decide to sell it to claim the $3,000 loss on your 2024 taxes. If you accidentally repurchase that same stock within 30 days, the IRS disallows the loss. You’re stuck with that loss until you sell the stock again, and now you’ve missed out on an immediate tax deduction.

By waiting out the 30-day period, though, you lock in the loss and can use it to offset other gains, or deduct $3,000 from your ordinary income. So, if you’re in the 40.8% tax bracket, this could save you up to $1,224 in taxes—just for sticking to the rule.

Let us understand this with an example –

Imagine you’re sitting on a portfolio where some of your stocks have tanked this year. The temptation might be to sell them off to lock in the losses and immediately jump back in at a lower price. But that’s where the wash-sale rule can trip you up.

Let’s say you sell a stock on December 15, and you buy the same stock again on December 25 because you believe it’s going to rebound soon. Since this repurchase happens within the 30-day window, the IRS will not allow you to claim the loss on your taxes. You’ll have to carry the loss over to the new stock’s cost basis, meaning no immediate tax break for 2024.

However, if you waited until, say, January 16 to buy the stock back, you could claim the loss for 2024 and still re-enter the market. Yes, you might miss out on some short-term gains during that 30-day period, but the tax savings could be worth it—especially if your loss was large enough to offset some big capital gains.

Limitations of Avoiding the Wash-Sale Rule

While avoiding the wash-sale rule can save you on taxes, there are some downsides and the biggest limitation is you have to sit out of the market for 30 days. That’s not always easy, especially if the stock you sold starts climbing back up during that period.

Here’s a scenario: Imagine you sold your stock for a $3,000 loss and planned to buy it back after 30 days to avoid the wash-sale rule.

But what if the stock shoots up in value during those 30 days? You’re left in a tough spot.

You missed out on a quick rebound and might end up paying more to get back in—potentially negating the tax benefit of avoiding the wash-sale rule.

Additionally, while you wait out the 30 days, your money is sitting idle, not working for you. If the market moves upward quickly, this could cost you more than the tax savings you’re hoping for.

So, timing is everything. You’ll need to weigh the potential tax savings against the risk of missing out on gains during that waiting period.

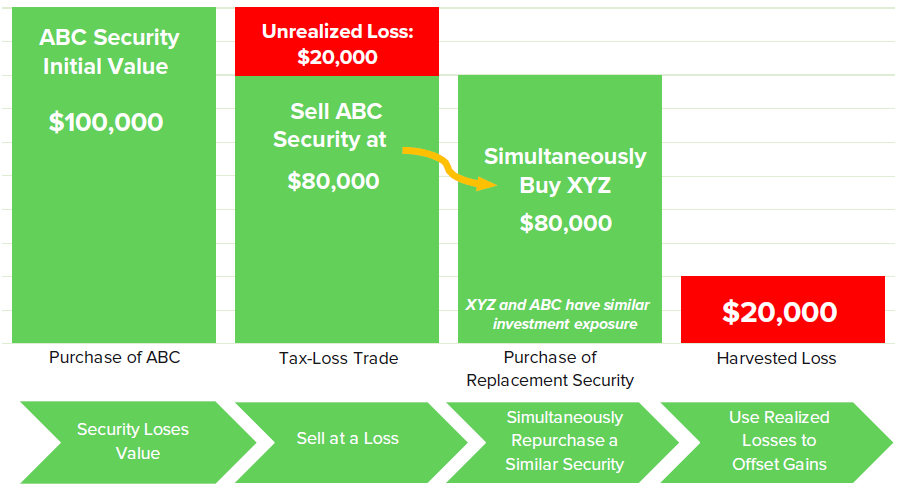

#Strategy 4. Sell Additional Assets to Use Excess Capital Losses

When you have accumulated more capital losses than you can immediately use, selling additional assets to take advantage of those losses is a smart move. This strategy helps you clear out any losses that exceed the annual $3,000 deduction limit. And unlike with losses, the tax code doesn’t impose a wash-sale rule on gains, so you can re-buy your assets without any restrictions. Let’s dive deeper into how this works, why it’s beneficial, and when it might not be the best fit for you.

Why Selling Additional Assets is a Game-Changer

When you’re sitting on hefty losses, the idea is to pair them with gains from other investments. Think of it like cleaning a house, by selling assets that have been appreciated, you can match your losses to the gains.

Here’s why this is a powerful tactic:

- No Wash-Sale Rule on Gains: While losses are subject to the 30-day wash-sale rule, there’s no such rule for gains. You can sell an appreciated stock today, claim the gain to offset your losses, and immediately buy back the stock if you want to keep it in your portfolio.

- Free Up Capital: This approach helps you rebalance your portfolio and get rid of underperforming stocks or assets that have hit their peak. You get the benefit of realizing the gains without the added tax hit, as your losses will neutralize the taxes on those gains.

So how can you turn your losses into tax relief, let’s understand with an example:

Let’s say you’ve got $15,000 in capital losses for 2024. You’ve already applied $3,000 to offset your ordinary income (the annual limit), but you’ve still got $12,000 in losses hanging around. Here’s where the strategy kicks in:

Imagine you own a rental property or stock with $12,000 in gains. By selling that asset, you can use your excess losses to completely offset the gain—meaning you pay zero taxes on that sale. In the end, you will see that you have essentially erased what could have been a tax bill on $12,000 worth of profit.

This is perfect if you’ve got a mixed bag of investments, some up, some down, and want to ensure you’re not paying more in taxes than necessary.

Additional Benefits: Rebalancing and Flexibility

One added bonus of this strategy is that it allows you to rebalance your portfolio. By selling appreciated assets, you can readjust your portfolio’s composition to better match your financial goals without worrying about the tax consequences. Plus, you’re not locked out of re-buying the asset. If you still believe in the long-term potential of the stock or property, you can get back in without triggering a penalty like you would with the wash-sale rule.

Also, if you’ve got capital loss carryovers from previous years, this is an excellent way to finally put them to work. It can feel frustrating sitting on unused losses, but by realizing gains through additional asset sales, you turn those losses into real tax benefits.

Limitations: When Selling Additional Assets Might Not Work

While this strategy offers some great advantages, it’s not always a perfect fit for everyone. There are a few things to keep in mind before diving in:

- Locking in Gains Could Backfire: If you’re selling assets purely for the tax benefit but the asset is set to continue appreciating, you could be missing out on future profits. It’s important to only sell assets that you’re okay with parting ways with or that have reached a point where further growth is unlikely.

- State Taxes Can Add Complexity: Depending on where you live, state taxes might complicate things. While federal rules allow for offsetting gains with losses, state tax laws might not be as generous. You could end up in a situation where you’re still paying state taxes on the gains, even if you’ve wiped them out federally.

- Market Timing Risks: Let’s say you sell a stock to realize a gain and plan to repurchase it immediately. If the market is particularly volatile, you run the risk of buying it back at a higher price, which could negate some of the tax benefit you just gained.

For example –

Imagine selling $12,000 in stock gains to offset your losses, and then the stock price soars by 20% shortly after. Sure, you’ve reduced your 2024 tax bill, but you also missed out on a potential $2,400 profit by selling too soon. In this case, you might have been better off holding onto the stock and letting your capital losses carry forward for future years when you have fewer gains.

Exploring a Balanced Approach

So, should you always rush to sell assets to offset your capital losses?

Not necessarily. It’s about balance. If you’ve got assets that have appreciated but are unlikely to grow further, this strategy makes perfect sense. You wipe out your taxable gains and avoid a bigger tax bill.

But if you think those stocks or properties will keep growing, it might be worth holding onto them and carrying over the loss to future years.

#Strategy 5. Gift Appreciated Stock to Family Members in Lower Tax Brackets

Gifting appreciated stock to family members in lower tax brackets can be a smart move when it comes to reducing your overall tax burden. It’s a win-win—you get rid of stock that has gained value and avoid paying hefty capital gains taxes, while your family members receive the gift and pay lower taxes when they sell it. Let’s break it down to understand why this strategy works so well and what you need to watch out for.

Why It’s Beneficial

When you gift appreciated stock to someone in a lower tax bracket, they sell the stock at their lower tax rate. Meanwhile, you avoid paying the higher tax rate you’d owe if you sold the stock yourself. This means you’re shifting the tax burden to a family member who is taxed at a lower rate, ultimately saving your family money.

- They Pay Less: For instance, if you’re in the highest capital gains bracket at 23.8%, and your parent or child is in the 0% or 15% bracket, they’ll pay much less when they sell the stock.

- Avoid the Hit: Instead of paying taxes on the stock appreciation, you transfer the value to someone else who can sell it at a lower tax cost. It’s a tax-efficient way to help them out while cutting down your own tax bill.

Taken for an example-

Let’s say you own stock you bought for $5,000 a few years ago, and it’s now worth $20,000. That’s a $15,000 gain sitting in your portfolio. If you sell it, you’ll owe 23.8% on that $15,000 gain, which is around $3,570 in taxes.

But, what if your parent is retired and only earning a small income, placing them in the 0% capital gains tax bracket? You can gift them the stock. When they sell it, they pay 0% on that same $15,000 gain. That’s $3,570 you would’ve paid that your parent doesn’t have to. You get to help them financially while sidestepping the big tax hit.

It’s like transferring the tax bill to someone who doesn’t have to pay it, leaving more money in the family’s pocket.

The Limitations

Of course, there are some limitations to this strategy, and it’s not a perfect fit for every situation. For one, you need to make sure your family member is truly in a lower tax bracket. If they’re in a similar bracket to yours or have other income that could bump them into a higher one, this strategy loses its shine.

- Kiddie Tax Trap: If you’re thinking about gifting stock to your child, be aware of the kiddie tax. This tax applies to children under 24 who are still students, meaning they’ll be taxed at your rate on unearned income over a certain amount (like capital gains from stock). So, if your child is still subject to the kiddie tax, this plan might backfire, and you could end up with no real tax savings.

- Gift Tax Exemption: You also have to watch out for gift tax rules. You can gift up to $17,000 per person in 2024 without triggering the federal gift tax. If you go over that amount, it eats into your lifetime exemption, which could affect your estate planning. That being said, most people don’t hit the lifetime exemption, but it’s something to keep in mind if you’re making large gifts.

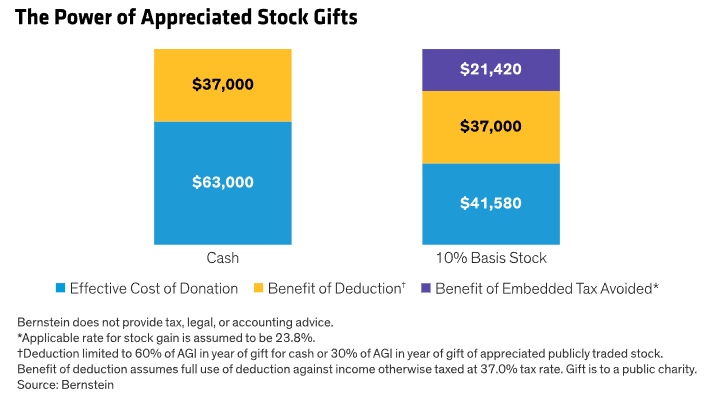

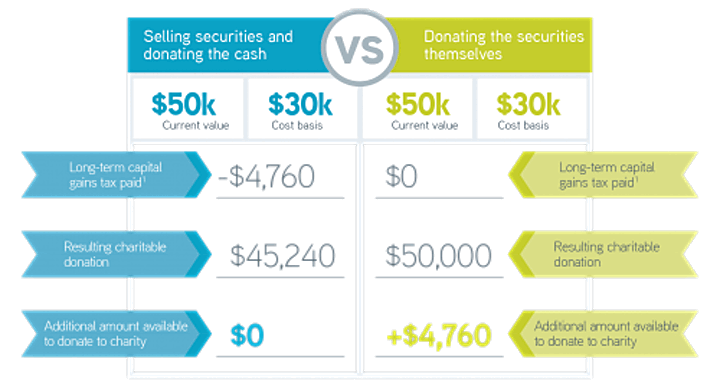

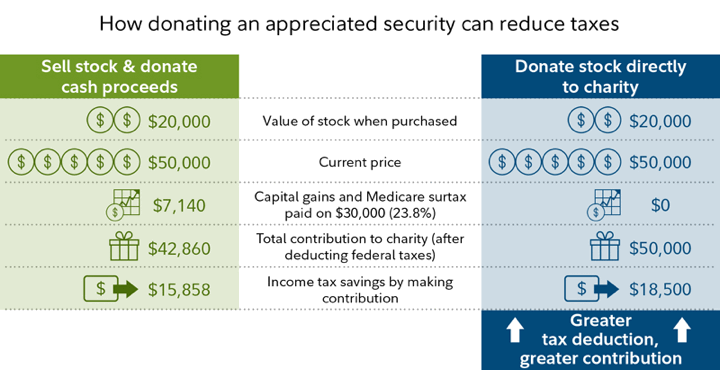

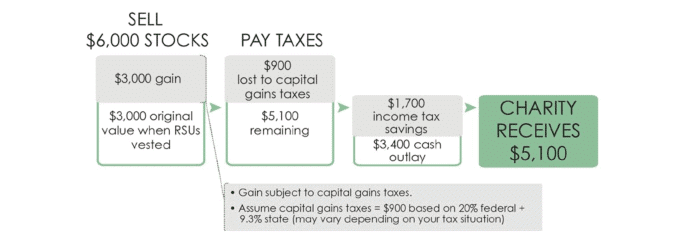

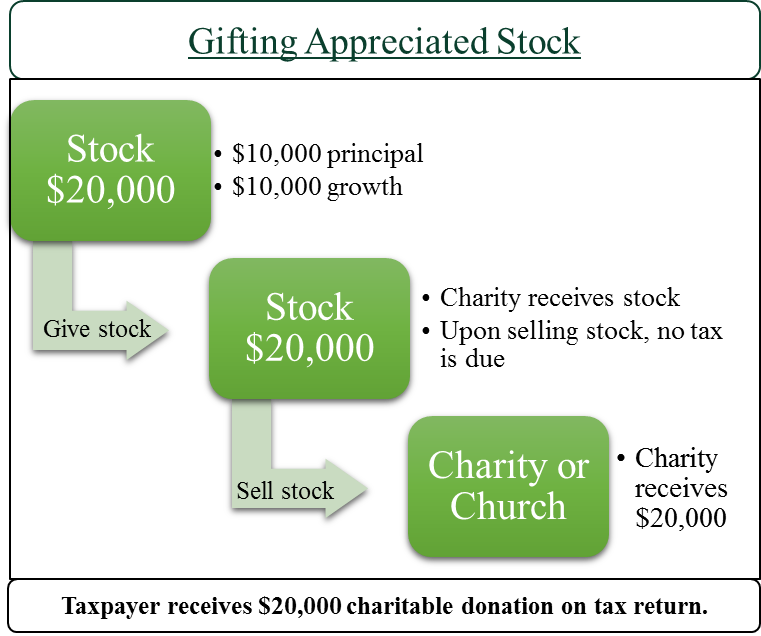

6. Donate Appreciated Stock to Charity for Maximum Tax Benefit

Donating appreciated stock to a charity instead of cash can be one of the most rewarding—and tax-savvy—ways to give. If you’ve held onto stocks that have grown significantly in value, this strategy not only supports the causes you care about but also saves you a lot in taxes. Let’s break it down and see why this can be such a win-win move.

The Double Benefit: Bigger Deduction, Zero Capital Gains Tax

When you donate appreciated stock, you unlock two major tax advantages.

First, you get to deduct the full fair market value of the stock at the time of donation, even if it’s grown significantly since you bought it. That means if you paid $1,000 for a stock and it’s now worth $11,000, you get to claim an $11,000 deduction on your taxes—not just the $1,000 you initially invested.

Second, you avoid paying capital gains taxes on the appreciation. Normally, if you sold that $11,000 stock, you’d have to pay taxes on the $10,000 gain. But by donating it directly to a charity, the charity can sell it without paying taxes, and you walk away with zero capital gains tax liability. It’s a total tax bypass!

Example: How It Works

Let’s say you bought stock for $5,000 a few years ago, and it’s now worth $15,000. If you decide to donate that stock to a 501(c)(3) charity, here’s what happens:

- You get a deduction for the full $15,000 on your tax return.

- You don’t have to pay capital gains tax on the $10,000 appreciation. Normally, if you sold it, you’d be hit with up to a 23.8% tax on that $10,000 gain, which comes out to $2,380. But by donating, you avoid that tax completely.

This means that you not only get a larger deduction than if you donated cash, but you also save thousands by skipping the capital gains tax.

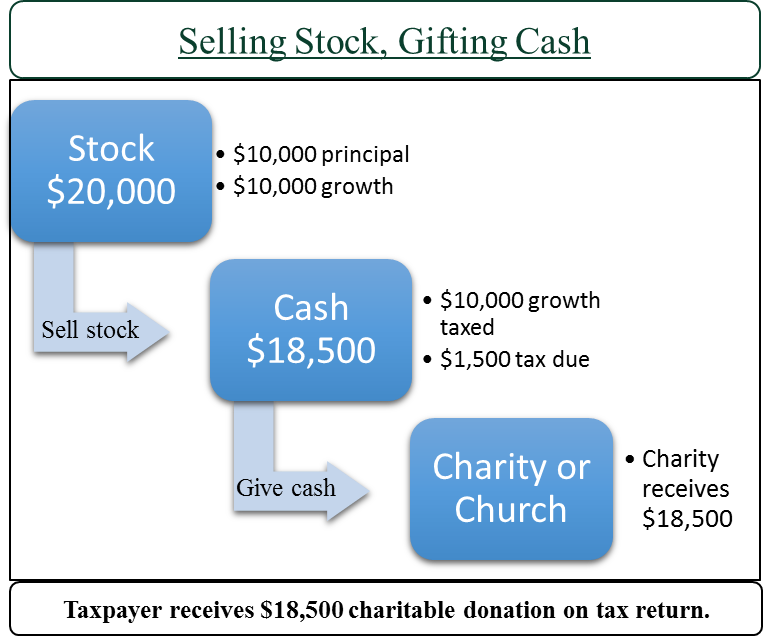

Why This Strategy Beats Cash Donations

Let’s compare donating stock versus just writing a check. If you sold the stock for $15,000 and then donated that cash, you’d still get the same $15,000 deduction for the charitable donation. But—here’s the catch—you’d have to pay that $2,380 capital gains tax first. So, in reality, you’d only be donating about $12,620 after taxes.

By donating the stock directly, though, you avoid that tax hit, making the donation much more powerful and keeping your wallet happy.

Limitations and Things to Watch Out For

Now, while donating appreciated stock has serious upsides, there are a few limitations to keep in mind.

- AGI Cap on Deductions: Your deduction for donating appreciated stock is limited to 30% of your adjusted gross income (AGI). So if your AGI is $100,000, the most you can deduct in one year from appreciated stock donations is $30,000. But don’t worry—if your donation exceeds this limit, you can carry the excess deduction forward for up to five years.

- Holding Period: To get the full tax benefits, you need to have held the stock for at least one year. If you donate stock you’ve held for less than a year, the deduction is only for the cost basis (the amount you paid for the stock), not the fair market value. So, if you bought a stock for $1,000 and it’s now worth $5,000, you’d only be able to deduct $1,000 if you donate it within a year.

- Don’t Donate Losses: As mentioned earlier, donating stocks that have lost value doesn’t give you the same advantage. If you’re sitting on a loss, it’s much better to sell the stock first, use the loss to offset other gains (or take the $3,000 deduction against ordinary income), and then donate the proceeds.

There you have if, If your goal is to maximize your tax savings, donating appreciated stock can be an absolute game-changer. It allows you to give more to charity while simultaneously trimming down your tax bill.

7. Don’t Donate Loss Stocks to Charity

Donating to charity is always a feel-good move, but when it comes to giving stocks that have dropped in value, you need to pause and think about the tax angle. If you’ve got stocks sitting in your portfolio that are worth less than what you paid for them, giving them directly to a charity might sound generous, but it’s not the best financial move.

Here’s why—and what you should do instead.

Sell the Stock First, Then Donate

If you donate a stock that’s lost value, you miss out on a key tax benefit: the ability to claim the loss. Let’s break it down. When you sell a stock for less than you paid, you can deduct that loss from your taxes. This is huge because you can use that loss to offset gains elsewhere in your portfolio, or even deduct it from your ordinary income (up to $3,000 per year).

Now, if you skip the selling step and simply donate the stock directly to charity, guess what? You don’t get to claim that loss. It’s like throwing a potential tax break out the window.

Understand with an Example Why Selling First is Better

Let’s say you bought some stock for $5,000 but today, it’s only worth $2,000. If you sell the stock, you can claim a $3,000 loss on your taxes. That $3,000 loss can either:

- Offset other capital gains (if you’ve got any), reduce your overall tax bill, or

- Deduct from your ordinary income if you’re short on gains, giving you up to a $3,000 tax break this year.

Once you’ve sold the stock and captured that loss, you can take the $2,000 proceeds and donate it to your favourite charity. Now you’ve unlocked two tax benefits:

- You’ve deducted the $3,000 loss from selling the stock.

- You get a tax deduction for donating the $2,000 cash to the charity.

It’s a win-win. You’ve turned a losing stock into a double tax break.

But … Of course, this strategy has also its limitations.

First off, if you don’t have any gains to offset, the impact of the loss might not be as significant. You can still use up to $3,000 of the loss to deduct from your ordinary income, but if you’ve got larger losses, the rest will carry over to future years.

Another thing to consider is that this strategy requires a bit of extra work. You need to sell the stock first and then donate the proceeds. It’s not complicated, but it’s an extra step that some people might overlook in their rush to meet year-end tax deadlines.

Why You Shouldn’t Just Donate the Stock

It’s tempting to take the easy route and just donate the stock directly, especially if you’re in a rush. But if the stock has dropped in value, you’re missing out on a valuable tax deduction. By selling the stock first, you keep control over the tax situation. You’re making sure you capture that loss, and then you can still follow through on your charitable goals by donating the proceeds.

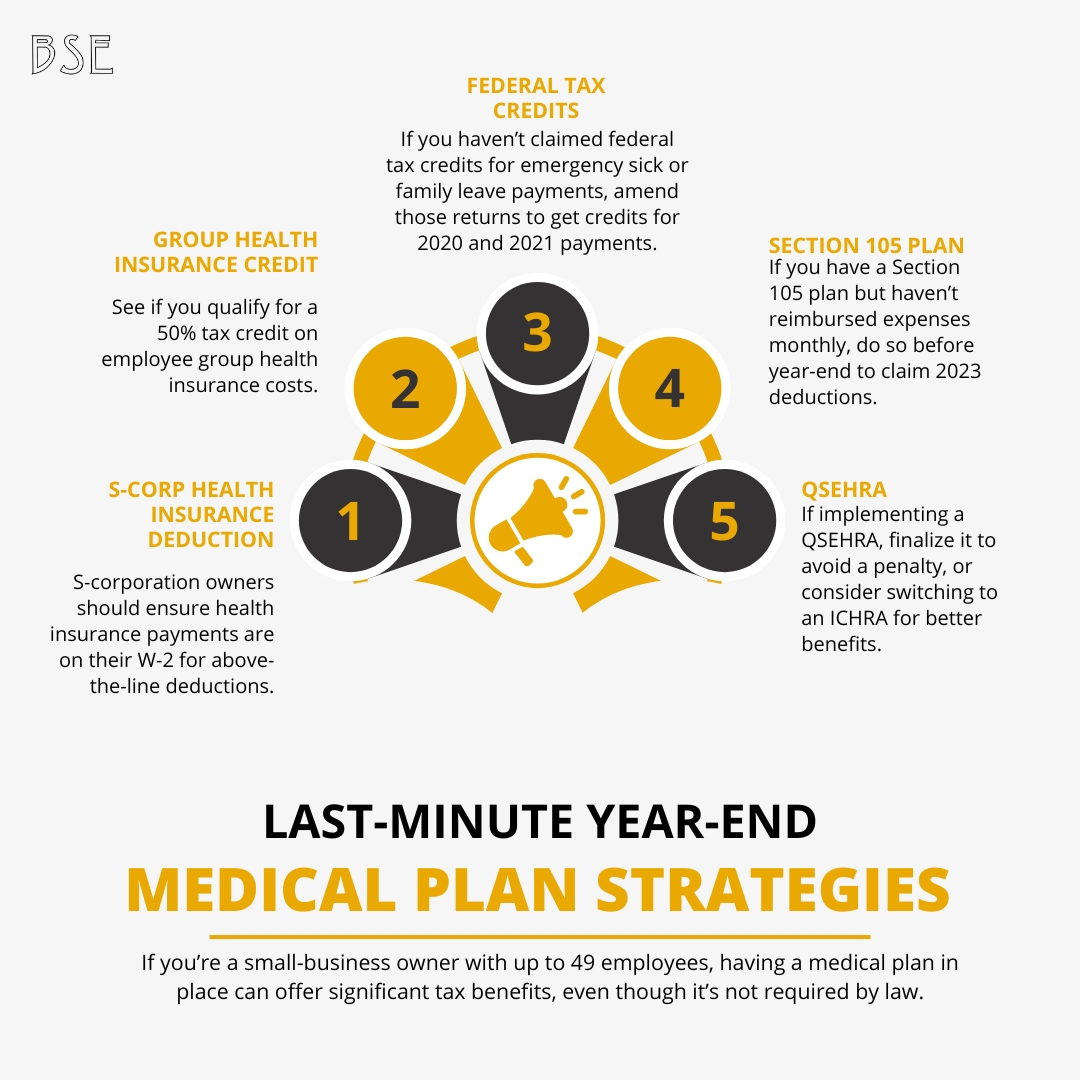

Last-Minute Year-End Medical Plan Strategies for 2024-2025

As a small business owner with up to 49 employees, providing a medical plan for your team isn’t just a good idea—it’s a smart business strategy. While current tax law doesn’t mandate you to offer a plan, having one in place brings valuable benefits, including potential tax savings, improved employee morale, and an edge in talent retention.

Many business owners are unaware of the tax credits and savings that can be leveraged by structuring their medical plans efficiently. Here are six must-know strategies to maximize your medical plan’s tax benefits before the year ends.

1. Claim the Federal Tax Credits for Emergency Sick and Family Leave Payments

Did you know the IRS provides tax credits for employers who made emergency sick leave and family leave payments? If your business made these payments in 2020 or 2021 and you haven’t claimed the credits yet, you might be leaving money on the table.

The federal government provided a 100% tax credit for both required and voluntary payments made during the pandemic. This means if your business compensated employees for time off due to COVID-19-related reasons, those payments could qualify for tax relief.

Even though the pandemic feels like a distant memory, the tax credits are still valid. By amending your previous returns, you can reclaim significant savings that directly impact your 2024 taxes. Time is of the essence—consult with your tax professional today and review the IRS guidelines on emergency leave credits to ensure you’re not missing out on these crucial benefits.

Pro tip: Go through your payroll records carefully. If you paid employees for emergency leaves and forgot to claim the credit, you can amend your tax returns up to three years after the original filing date.

2. Maximize Your Section 105 Plan with End-of-Year Reimbursements

A Section 105 plan allows you to deduct medical reimbursements and lower your taxable income. If you have such a plan in place but haven’t been reimbursing expenses monthly, now is the time to catch up and lock in those deductions for 2024.

To ensure that your reimbursements are compliant with IRS rules, make a final lump sum reimbursement for 2024 before December 31. This step will allow you to capture eligible medical expenses for the year and include them in your deductions. Once you’ve done this, set up a monthly reimbursement schedule for 2025 to make the process easier and more tax-efficient moving forward.

Have trouble keeping track of reimbursable expenses?

You’re not alone. ….

Many small business owners struggle with this, which is why it’s crucial to implement a streamlined system for tracking medical expenses. A Section 105 plan allows deductions not only for insurance premiums but also for out-of-pocket medical expenses, ensuring that you don’t overpay in taxes.

Tip: For owners of S-corporations, the rules are slightly different, so always consult with a tax professional to ensure compliance.

BOOK YOUR FREE CONSULTATION NOW

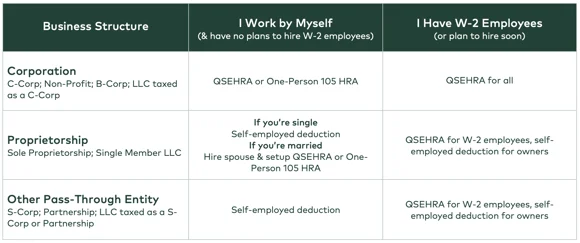

3. Implement a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

If you’re looking for a flexible way to offer health benefits to your employees, implementing a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) is a great option. But be cautious—you need to set it up correctly before the end of the year to avoid penalties.

QSEHRAs allow you to reimburse employees for their individual health insurance premiums and other medical expenses. Employees love this option because it gives them the freedom to choose their own plans, and you get to control costs. However, missing the setup deadline could result in penalties of up to $50 per employee per day, which adds up quickly.

Late to the game? Not all is lost! You can still implement a QSEHRA for 2024 if you act fast and make sure it’s done by December 31. Keep in mind that QSEHRAs have contribution limits ($5,850 for individuals and $11,800 for families in 2024), so plan accordingly.

Check the IRS QSEHRA regulations to ensure you’re staying within legal limits and requirements.

4. Consider an Individual Coverage Health Reimbursement Arrangement (ICHRA)

If flexibility and greater control are what you’re after, an Individual Coverage Health Reimbursement Arrangement (ICHRA) may be a better fit than a QSEHRA. ICHRA allows you to offer a more tailored solution with greater allowances for employee coverage while offering tax savings for your business.

Unlike the QSEHRA, the ICHRA doesn’t have contribution limits, making it a more flexible option if you want to provide more substantial reimbursement for health-related expenses. This arrangement allows employees to select individual plans and be reimbursed for premiums, giving them more control and enabling you to retain top talent by offering valuable health benefits.

Setting up an ICHRA for 2024 requires timely action. You must notify employees and have everything in place by the end of the year to reap the benefits. Not sure whether ICHRA is right for your business? Compare it against your existing health benefit strategy and consult the official IRS guidelines on ICHRA to make an informed decision.

5. Get Your S Corporation’s Health Insurance Deductions Above the Line

If you operate your business as an S corporation, you’ve got some extra steps to follow to claim a health insurance deduction on your personal Form 1040. But the effort is worth it—getting this right can save you a significant amount in taxes.

For 2024, to claim the above-the-line deduction, your S corporation must (1) pay for or reimburse your health insurance premiums and (2) include those amounts on your W-2 form as taxable income. This needs to be done before December 31 to ensure your eligibility.

Once these steps are completed, you’ll be able to claim the deduction directly on your Form 1040, reducing your personal taxable income. It’s a win-win situation—you maintain compliance, and you get tax savings.

Key takeaway: Make sure your health insurance reimbursement happens before year-end and the expense is properly reported on your W-2 form. Failure to do so will result in lost deductions, costing you more in taxes.

6. Claim the Small Business Health Care Tax Credit

The Small Business Health Care Tax Credit offers a substantial tax break for qualifying employers. If you provide group health insurance to your employees, you could be eligible for a tax credit worth up to 50% of the premiums you paid for 2024.

To qualify, your business must meet specific criteria, including having fewer than 25 full-time equivalent employees, paying an average wage of less than $59,000 per year, and covering at least 50% of employee health insurance premiums.

If your business qualifies, you can claim this credit on your year-end tax return, reducing the overall cost of offering health benefits. And don’t forget—this credit can be applied retroactively for previous tax years, so it’s worth reviewing your prior filings to ensure you didn’t miss out.

For more information, visit the IRS Small Business Health Care Tax Credit page to check if your company is eligible and learn how to claim the credit.

Last-Minute Year-End Retirement Deductions for 2024-2025

As the year-end approaches, it’s crucial to maximize retirement contributions and reduce tax liabilities. With a few strategic moves before December 31, you can set yourself up for future financial success. Let’s explore five tax-saving strategies for 2024-2025.

1. Establish Your 2024 Retirement Plan

If you haven’t set up your 2024 retirement plan yet, you’re missing out on a major opportunity to save both for your future and on taxes. Let’s break down why establishing your retirement plan before the end of the year is essential, how it can benefit you, and what limitations you should be aware of.

The Benefits of Setting Up Your Plan

Setting up a retirement plan for 2024 can yield significant tax benefits. For instance, if you’re a business owner or self-employed, you can contribute as both the employer and the employee. This gives you a dual advantage by allowing for larger contributions than most people realize.

Here’s a real example of how it works:

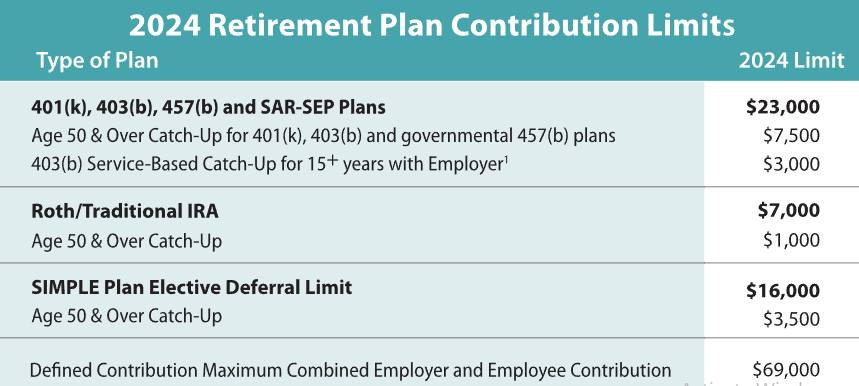

Let’s say you’re a business owner with a solid income. You can contribute up to $66,000 in 2024 under a 401(k) plan, combining both the employer and employee portions. That’s a massive boost to your retirement savings and a corresponding reduction in your taxable income. Plus, by putting away more in tax-advantaged accounts, you lower your current tax bill while building a nest egg for the future. Win-win!

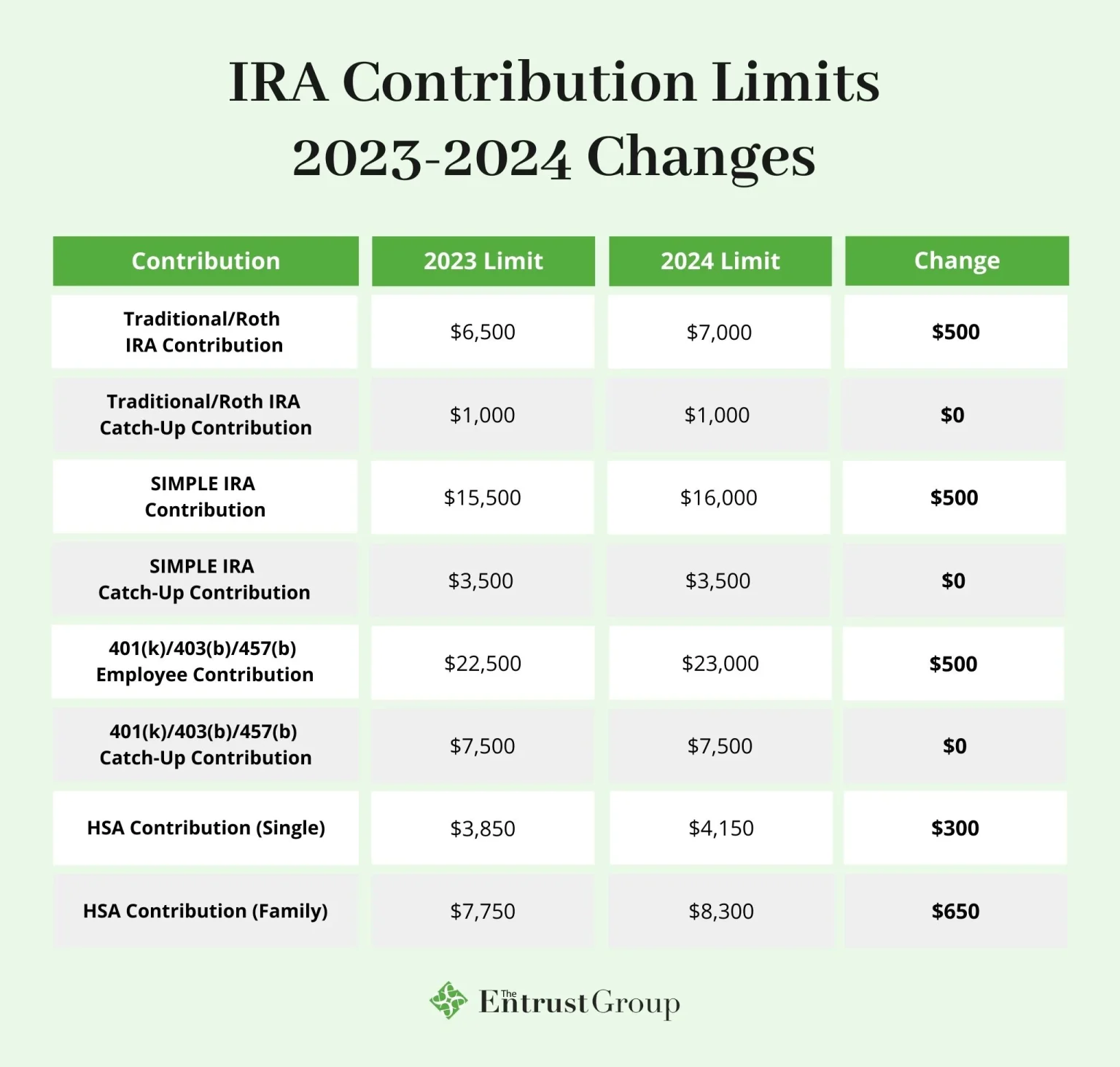

Another benefit of setting up your retirement plan now is the ability to make catch-up contributions if you’re over 50. In 2024, this catch-up contribution limit for a 401(k) is an additional $7,500, allowing you to contribute a total of $73,500 if you’re 50 or older. This is huge for those who may have started saving late and need to accelerate their retirement savings.

And it’s not just about tax deductions. Establishing a retirement plan, especially for a business, also helps attract and retain quality employees. Offering a 401(k) or SEP IRA plan with employer contributions can make your company more appealing to potential hires and boost employee satisfaction.

Limitations to Consider

While the benefits are substantial, it’s important to note some limitations. For example, not all businesses or individuals can contribute the maximum amount every year. Your income level plays a crucial role in determining how much you can contribute. If your business had a slow year, you may not be able to contribute as much as you’d like, limiting the tax deduction.

Another limitation is administrative complexity. Setting up a 401(k) or a more advanced plan like a defined benefit pension plan can involve administrative fees, paperwork, and ongoing maintenance costs. These costs can eat into the financial benefits of the plan, especially for small businesses with limited cash flow. So, if your company isn’t ready to shoulder these extra expenses, it might be better to start with something simpler, like a SEP IRA or a SIMPLE IRA, both of which have lower administrative costs.

How It’s Beneficial Despite Limitations

Even with these limitations, the advantages often outweigh the drawbacks. For instance, if you have a small business and can’t contribute the maximum amount every year, you still benefit from the contributions you make. Let’s say you contribute $30,000 instead of the full $66,000 in 2024. That’s still $30,000 you’ve shielded from taxes, plus it’s growing tax-deferred in your retirement account. This deferral alone can save you thousands of dollars in taxes every year.

For example, if you’re in a 32% tax bracket, that $30,000 contribution could save you close to $9,600 in taxes this year. Now, imagine if you had opted not to set up a retirement plan at all—you’d be paying that extra $9,600 to the IRS instead of funnelling it into your future financial security.

2. Leverage the Retirement Plan Start-Up Tax Credit (Up to $15,000)

Starting a new retirement plan for your small business comes with fantastic tax benefits, thanks to the Retirement Plan Start-Up Tax Credit. For 2024, you can earn a credit of up to $15,000 over three years, making this one of the most valuable incentives for small businesses looking to support their employees’ futures while saving on taxes.

How Does the Credit Work?

Let’s break it down. The credit applies to qualified start-up costs, which include the expenses associated with setting up and administering the retirement plan, along with educating your employees about it. For the first three years, the credit can be as high as 50% of these costs, with a cap of $5,000 per year.

But wait, it gets better. If you add an automatic enrollment feature to your plan, which encourages employee participation, you can tack on an additional $500 per year for up to three years, bringing the potential total to $15,000.

Why Is This Credit Beneficial?

This tax credit isn’t just free money from the government—it’s a powerful way to reduce costs when offering retirement benefits. By setting up a retirement plan, you’re attracting and retaining top talent, increasing employee satisfaction, and improving your company’s competitive edge.

For small business owners, cash flow can be tight, so every dollar saved matters. This credit effectively cuts the cost of establishing and maintaining a plan in half for the first three years, making it easier to get started without worrying about excessive up-front costs.

Example: How It Works in Real Life

Let’s say you’re a small business owner with 10 employees, and you decide to establish a 401(k) plan this year. You incur $4,000 in administrative costs and another $1,000 to provide educational materials to your team about the plan.

In this scenario, the IRS allows you to claim 50% of those costs, so you can deduct $2,500 from your tax bill just for getting the plan off the ground. If you include an auto-enrollment feature, you can add an extra $500 credit, bringing your total savings to $3,000 for the year.

And don’t forget—you can repeat this credit for the next two years, potentially earning a total of $9,000 over three years just for doing the right thing by your employees.

Limitations: When It Doesn’t Work in Your Favor

Of course, like any tax benefit, there are limitations to be aware of. One key limitation is that this credit is only available for small businesses with 100 or fewer employees. If your business grows beyond this, the credit phases out.

Additionally, the credit doesn’t cover all costs. For example, it only applies to 50% of your start-up costs, meaning you’ll still need to cover the other half. If you’re setting up a more complex retirement plan like a Defined Benefit Plan, the administrative costs can be significantly higher than with a simple 401(k) or SEP IRA, so even with the credit, there could be substantial out-of-pocket expenses.

Another catch is that this credit is non-refundable, meaning it can only reduce your tax liability to zero—it won’t result in a tax refund if the credit exceeds what you owe.

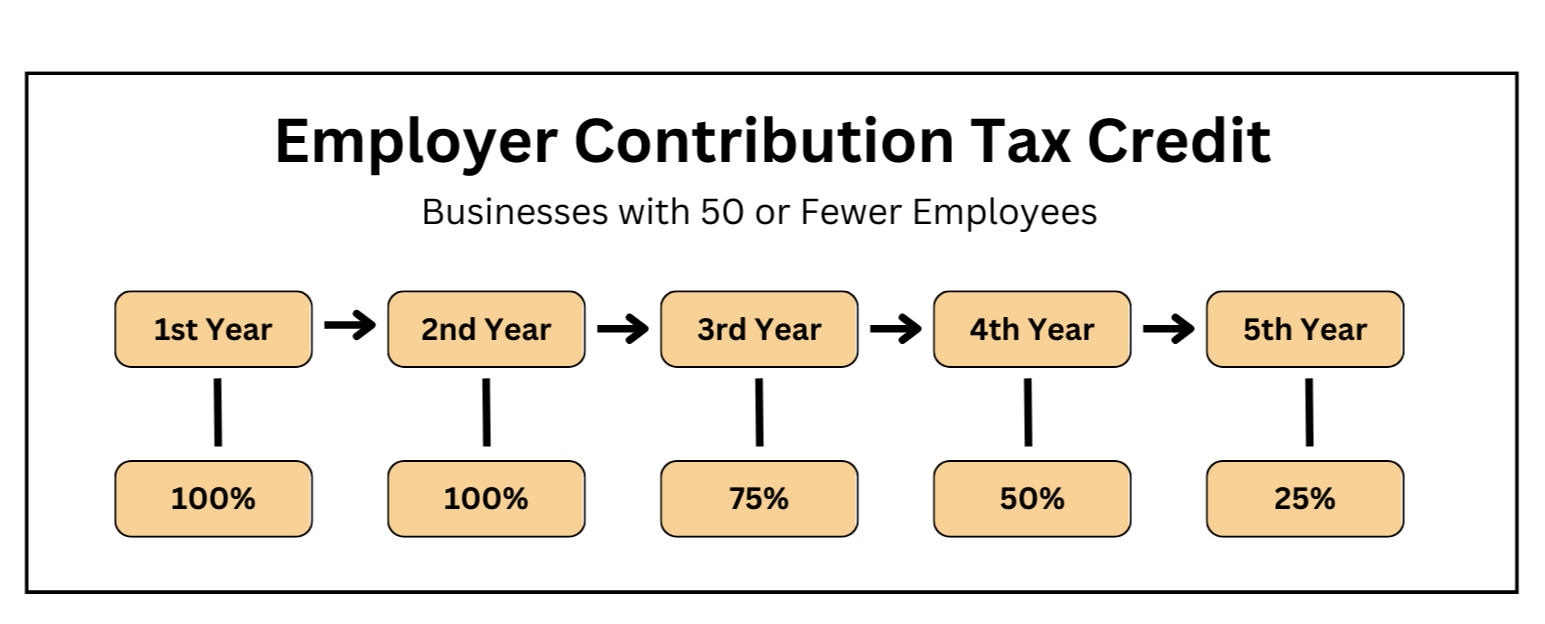

3. Claim the Small Employer Pension Contribution Credit:

The Small Employer Pension Contribution Credit is one of the most enticing benefits for small business owners. This credit is a game-changer because it rewards you for contributing to your employee’s retirement savings, offering financial relief while helping to secure their futures.

The Benefits: Encouraging Retirement Savings

Starting in 2024, you can claim up to $1,000 per employee for contributions you make to their retirement plans. This includes common plans like a 401(k), SIMPLE IRA, or SEP. The SECURE Act 2.0 extended this credit to help businesses cover the costs of retirement contributions, making it more financially feasible for small employers to offer these benefits.

Let’s break down why this credit is so helpful:

- Boost Employee Retention: Offering a solid retirement plan can help you keep your team happy. When employees see you’re investing in their future, they’re more likely to stick around. This credit makes it easier for you to support them without stretching your budget.

- Offset Costs: The credit directly offsets your costs, especially in the first two years. In year one, the credit covers 100% of your contributions (up to $1,000 per employee). By year two, it still covers the full amount, so if you contribute $500 to each employee’s plan, you get that $500 back through the credit.

- Long-Term Incentives: While the credit decreases in percentage over time (75% in year three, 50% in year four, and 25% in year five), it still allows you to ease into higher contributions without feeling the full financial burden right away.

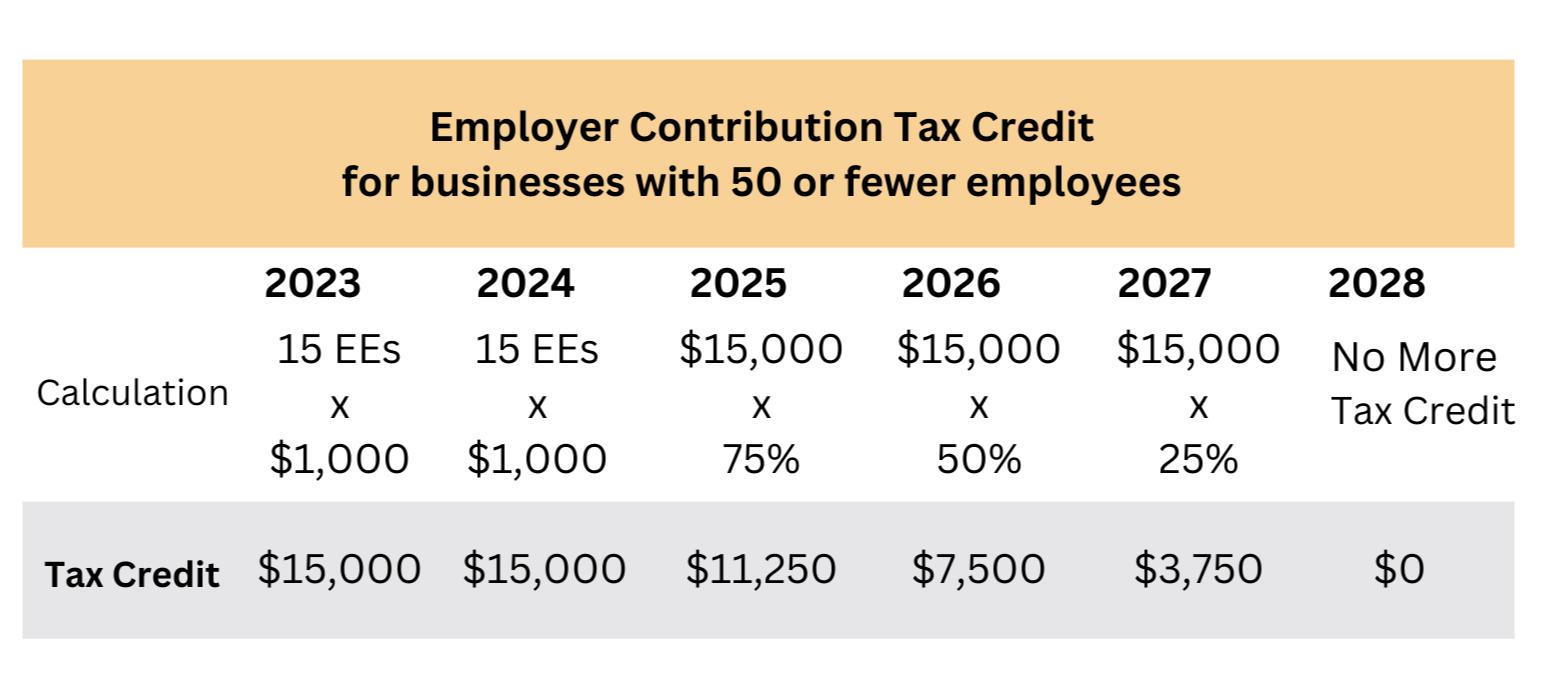

How It Works: A Real-World Example

Let’s imagine you run a small tech company with 20 employees. You’ve decided to set up a 401(k) retirement plan for your team, and you contribute $1,000 for each employee.

Year One: You contribute $20,000 ($1,000 for each of the 20 employees). Under the Small Employer Pension Contribution Credit, the IRS gives you a $20,000 tax credit to offset those contributions. This means you get back every dollar you contributed.

Year Two: You contribute the same amount ($1,000 per employee). Again, you get a credit for 100% of your contributions, so another $20,000 saved in taxes.

Year Three: Now, the credit starts to phase down. You contribute $20,000, but the IRS only gives you a 75% credit, so you receive $15,000 as a tax credit. While the benefit is smaller, you’re still getting significant relief.

Over the first three years, you’ve contributed $60,000 but received $55,000 in tax credits. This means you’ve only effectively paid $5,000 for your employees’ retirement savings. That’s a substantial return on investment!

Limitations: Not for Everyone

While this credit is highly beneficial, there are some limitations to consider:

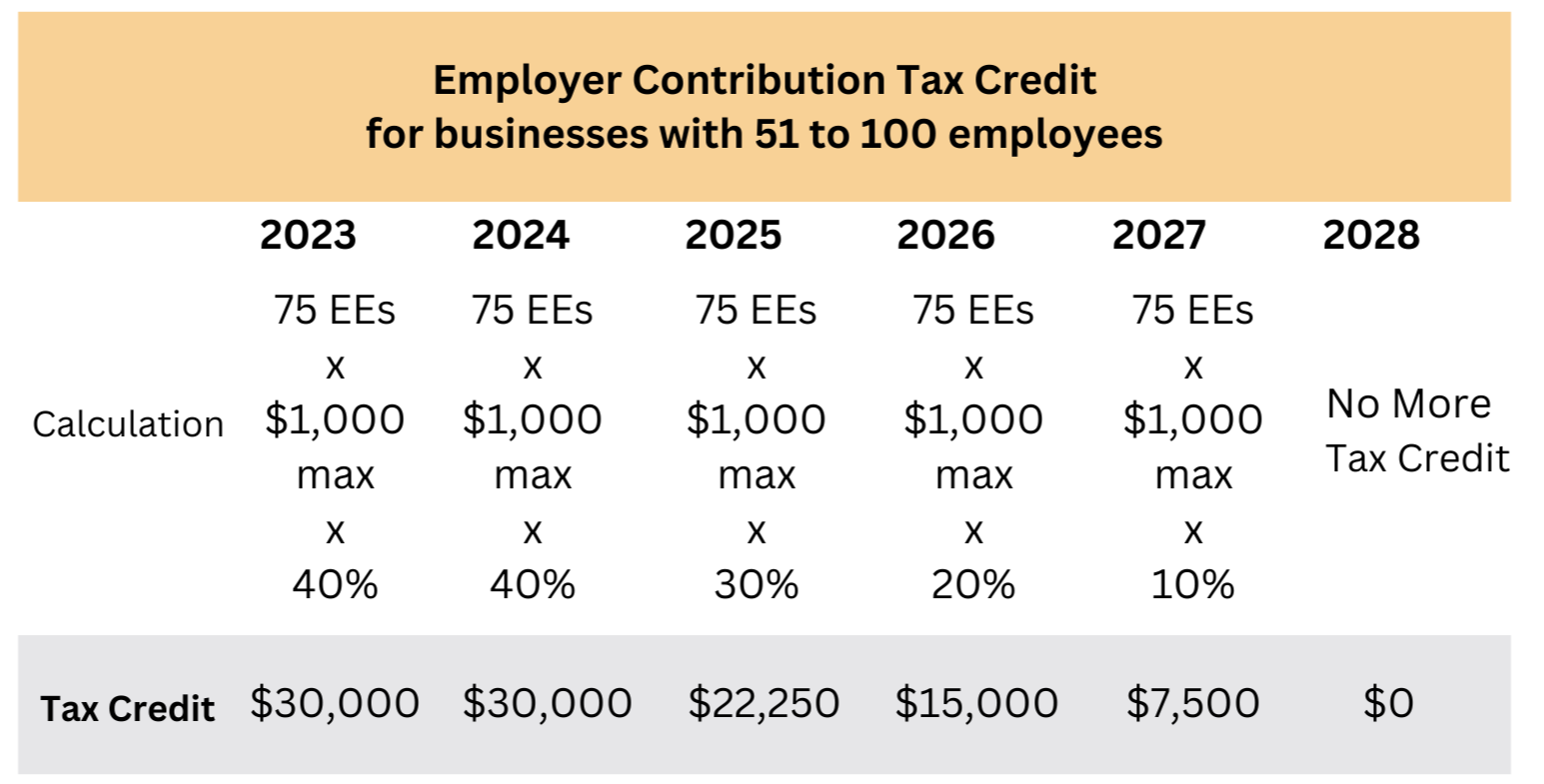

- Business Size Restrictions: The credit is designed for small businesses with fewer than 50 employees. Once your business grows beyond that, the benefit starts to phase out. For employers with 51-100 employees, the credit decreases by 2% for each additional employee over 50. If you have more than 100 employees, you won’t be eligible for the credit at all.

- Income Cap for Employees: There’s also an income restriction for the employees you’re contributing for. Any employee who earns more than $100,000 in 2024 doesn’t qualify for the employer contribution credit. So if your workforce is primarily higher-earning professionals, you won’t be able to claim the credit for them.

- Defined Benefit Plans: The credit doesn’t apply to defined benefit plans (like pensions), which can be a drawback for some businesses. If you’re contributing to these types of plans, the contributions won’t be eligible for this credit.

Why It’s Still Worth It

Despite these limitations, the Small Employer Pension Contribution Credit is a powerful tool for small businesses that want to offer competitive benefits without breaking the bank. It gives you a structured way to introduce retirement savings for your employees, with the bulk of the financial burden lifted in the early years. And even after the five-year mark, the benefits of contributing to a retirement plan—such as better employee retention and tax-deferred savings—still make it a worthwhile investment.

By taking advantage of this credit, you’re not just building your employees’ future; you’re securing financial relief for your business, too. It’s a win-win.

For more details, you can always check the IRS guidelines on the official website or refer to the Department of Labor.

4. Automatic Enrollment Tax Credit

Adding an automatic enrollment feature to your retirement plan not only simplifies the onboarding process for your employees but also comes with a handy incentive—an automatic enrollment tax credit of up to $500 per year for up to three years. This tax credit is designed to encourage small businesses to adopt automatic enrollment in plans like 401(k)s, making it easier for employees to save for retirement while providing some tax relief for the employer.

How the Credit Works

Beginning in 2024, eligible employers can claim this $500 tax credit each year for the first three years they implement automatic enrollment in their retirement plans. This means if you decide to add this feature to a 401(k) or SIMPLE IRA plan, you could be looking at a $1,500 tax credit over three years.

Example: Let’s say you run a small business with 25 employees and you introduce automatic enrollment in your 401(k) plan starting in 2024. By doing so, you will immediately qualify for a $500 tax credit in the first year, followed by another $500 for the next two years, even if the cost to add automatic enrollment is negligible. This tax relief can help offset administrative costs while boosting employee participation in the retirement plan.

Why Automatic Enrollment Is Beneficial

The benefits of automatic enrollment are twofold. First, it gets more employees involved in saving for their retirement, especially those who might otherwise procrastinate or forget to enrol. Research shows that auto-enrollment leads to higher participation rates, making it an effective tool for improving long-term financial security for workers.

From the employer’s perspective, automatic enrollment is a way to ensure your employees are taking advantage of retirement savings opportunities without needing constant reminders or nudging. It’s like giving your employees a gentle push towards their future financial stability while scoring a tax break.

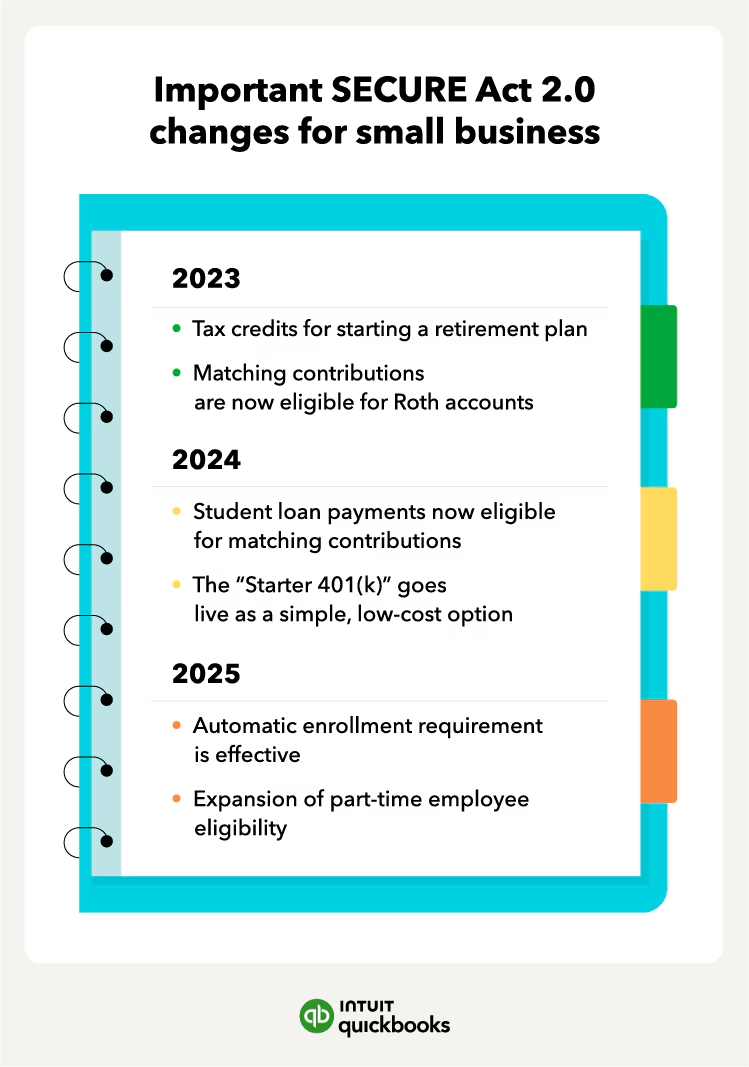

And there’s more—starting in 2025, the SECURE 2.0 Act mandates that new retirement plans must include automatic enrollment. By implementing it early, you’re not only staying ahead of compliance requirements but also benefiting from tax incentives.

Limitations and Considerations

While automatic enrollment is great for boosting participation, it’s not without limitations. The $500 tax credit is relatively small, and for larger businesses, this might not make a significant dent in costs, especially if the company already has a high participation rate or sophisticated retirement plans in place.

Additionally, automatic enrollment doesn’t mean employees are locked in—they can still opt out if they prefer not to participate. This could result in lower-than-expected participation rates for employers who are relying solely on auto-enrollment to boost engagement. Moreover, for businesses with limited payroll or financial flexibility, enrolling all employees into a retirement plan might create additional administrative complexity and costs.

However, despite these potential hurdles, the tax credit offers a win-win situation for businesses that are looking to grow employee participation in their retirement plans without taking a hit on taxes.

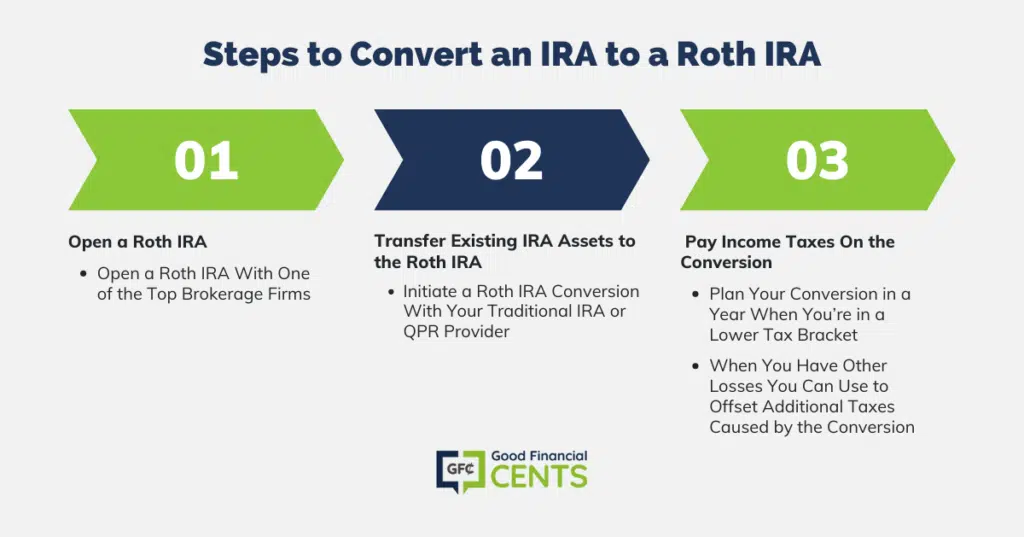

5. Convert to a Roth IRA

When you convert your traditional IRA or 401(k) to a Roth IRA, you’re making a move that could provide you with serious tax benefits down the line. Here’s why this conversion might be the right fit for you and how you can use it to your advantage:

Why Convert to a Roth IRA?

The Roth IRA has become a go-to strategy for many who want flexibility in their retirement savings. The big win with Roth IRAs is that all future withdrawals are tax-free. You pay taxes upfront when converting, but afterward, your money grows tax-free, and qualified withdrawals (after age 59 1/2 and holding the account for at least five years) aren’t taxed. This gives you a hedge against future tax increases, making a Roth IRA particularly valuable if you think your tax bracket might be higher when you retire.

Example of How It Works

Let’s say you have $100,000 in a traditional IRA. You convert that to a Roth IRA in 2024. The conversion amount adds to your taxable income for the year. If you’re in the 22% tax bracket, you’ll owe around $22,000 in taxes upfront. That may seem steep, but the long-term benefit comes when you start withdrawing from your Roth IRA during retirement—none of those withdrawals will be taxed.

Now imagine the Roth IRA grows to $300,000 by the time you retire. All that growth is tax-free! If you were in a higher tax bracket during retirement, like 28%, you just avoided paying a lot more in taxes on those future withdrawals.

The 2024 Change

Starting in 2024, Roth 401(k)s and Roth 403(b)s will no longer have Required Minimum Distributions (RMDs). This adds another layer of flexibility, meaning you can leave the money in your Roth account for as long as you want, allowing it to grow without being forced to withdraw at a specific age (like with traditional IRAs).

Limitations of a Roth IRA Conversion

But here’s the flip side—you need to be ready for the tax hit now. Converting a traditional account to a Roth IRA can bump you into a higher tax bracket for the year, especially if you’re converting a large amount. This is why it’s essential to consider if you have the cash on hand to cover the extra taxes.

Additionally, if you withdraw converted funds within five years of the conversion, you could face a 10% early withdrawal penalty on the taxable portion unless you’re 59 1/2 or older. Each conversion starts its own five-year clock, so keep this in mind if you’re thinking about withdrawing funds early.

How to Plan for the Conversion

To minimize the tax burden, consider spreading your conversion over several years instead of converting all at once. This can help keep you in a lower tax bracket while still benefiting from tax-free growth later on. Some people choose to convert only enough each year to avoid pushing themselves into a higher tax bracket.

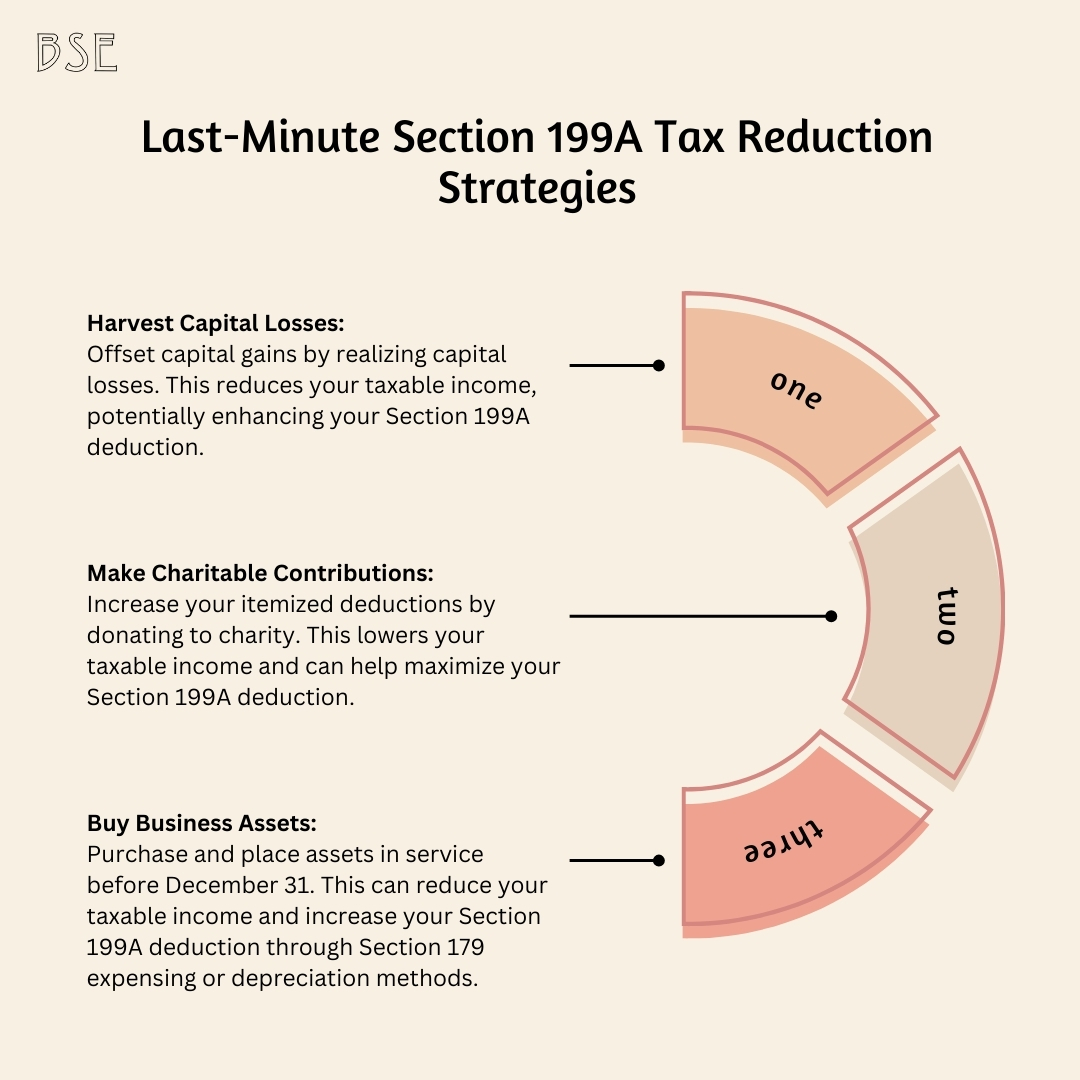

Last-Minute Section 199A Tax Reduction Strategies

When planning for the 2024 tax year, it’s essential to maximize your Section 199A deduction, especially as the end of the year approaches. Ignoring this deduction could lead to missing out on valuable tax savings. Here are three key strategies that can help you reduce your taxable income and boost your Section 199A deduction.

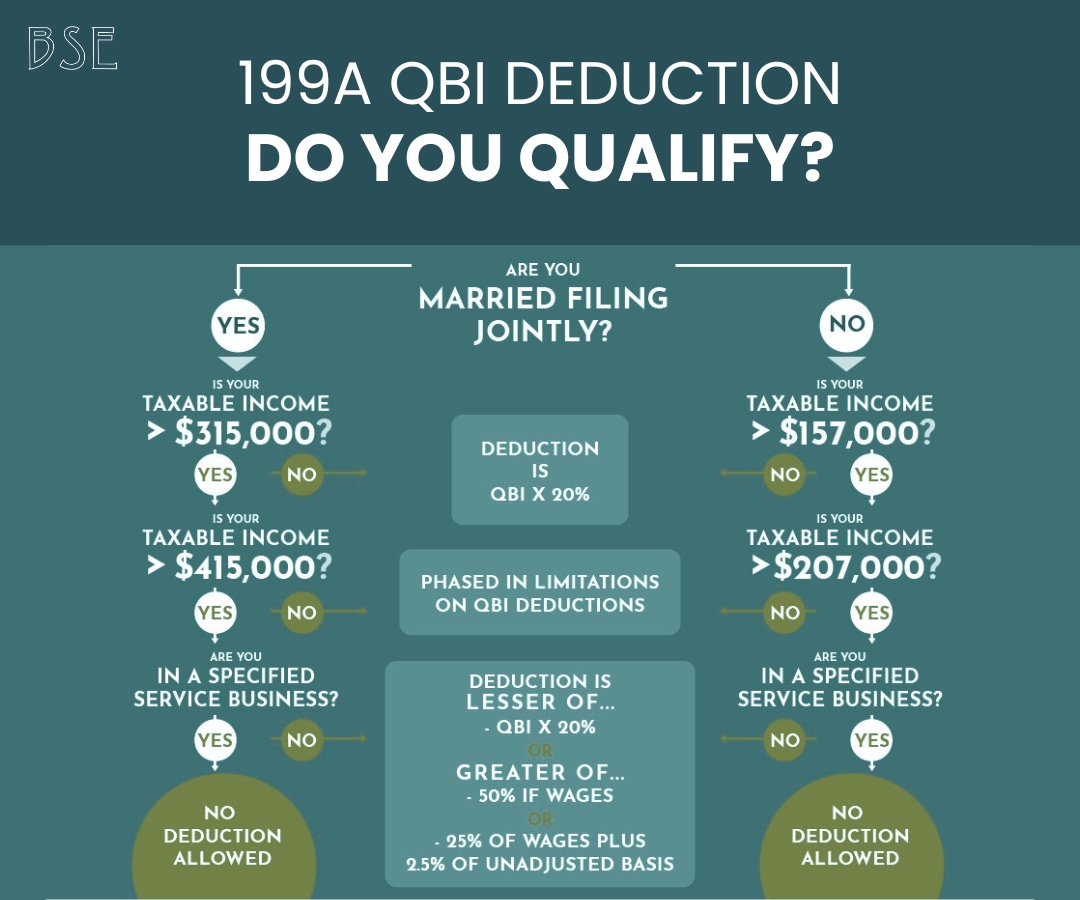

First Things First: Assess Your Taxable Income

For 2024, if your taxable income exceeds $190,050 for single filers or $380,100 for joint filers, certain limitations kick in that could impact your Section 199A deduction. Above these thresholds, factors like your business type, wages paid, and property owned can reduce or even eliminate the deduction.

If your deduction is falling short of 20% of your qualified business income (QBI), there are still strategies available to you before the year ends.

#Strategy 1: Harvest Capital Losses

Capital gains add to your taxable income, which impacts the size of your Section 199A deduction. Harvesting capital losses is one way to reduce this taxable income and optimize your deduction, especially in 2024. By realizing (or “harvesting”) losses on underperforming investments before the end of the year, you can offset gains and reduce taxable income, which in turn can increase your Section 199A deduction.

How It Works: An Example

Imagine you had a good year with your investments and accumulated $50,000 in capital gains, but you also have $20,000 in unrealized losses on other stocks. If you do nothing, your $50,000 capital gain is fully taxable.

Let’s say your taxable income, including the capital gains, is $390,000 (above the 2024 Section 199A threshold of $380,100 for joint filers). This means your Section 199A deduction will face limitations, possibly shrinking significantly.

However, if you sell those losing stocks and realize a $20,000 loss, your taxable capital gains are reduced to $30,000. This brings your taxable income down to $370,000, placing you back under the threshold. As a result, you might now be eligible for a larger Section 199A deduction, potentially up to the full 20% of your QBI.

Benefits Beyond Section 199A

Harvesting capital losses doesn’t just help with your Section 199A deduction. If your capital losses exceed your capital gains, you can also use the excess losses (up to $3,000 annually) to offset ordinary income, reducing your overall tax bill even further. Any losses that exceed this limit can be carried forward to future tax years, creating ongoing tax benefits.

In addition to increasing your Section 199A deduction, this strategy provides an opportunity to re-balance your investment portfolio without incurring a significant tax hit.

IRS Updates for 2024

For the 2024 tax year, the IRS has kept the basic rules for harvesting capital losses largely unchanged. You can still use realised losses to offset gains dollar-for-dollar, and if you have more losses than gains, the extra losses can offset up to $3,000 of ordinary income. The most important factor for the Section 199A deduction remains your taxable income, so reducing that income with capital losses is still a valid approach.

Limitations: When This Might Not Work

While harvesting losses sounds like a no-brainer, there are some situations where this strategy might not provide the desired benefits.

- Wash Sale Rule: If you repurchase the same or substantially identical security within 30 days of selling it for a loss, the IRS will disallow the loss under the wash sale rule. This can be a pitfall if you plan to reinvest quickly in the same assets.

- Minimal Losses: If your capital losses aren’t large enough to push your income below the Section 199A threshold, this strategy won’t have as big an impact on your deduction. For example, if you’re only slightly over the income threshold and your losses are small, the reduction in taxable income may be too minimal to improve your Section 199A deduction significantly.

- Future Capital Gains: Another consideration is that carrying forward too many losses into future years could reduce your ability to offset future capital gains, which may be taxed at favourable rates. In some cases, it may be more beneficial to accept higher taxable income in one year to preserve losses for future years when tax planning may be more complex.

#Strategy 2: Increase Charitable Contributions

Charitable contributions can be a win-win in your tax strategy. Not only do you get to support causes close to your heart, but it also directly reduces your taxable income — which is the critical figure when calculating your Section 199A deduction. The beauty of this strategy is how simple it is: if you’re itemizing deductions, you can increase those deductions just by giving more to charity. This directly affects your taxable income, helping you slide under the Section 199A income thresholds.

But let’s break this down with more clarity.

How Charitable Contributions Help

Charitable donations work because your Section 199A deduction is linked to your total taxable income. The IRS lets you deduct qualified charitable contributions from your taxable income, reducing the overall amount. By doing this, you’re potentially lowering yourself under the income threshold that caps your Section 199A deduction. The less taxable income you report, the higher the chance that you can maximize your 20% deduction.

For instance, if you’re teetering near the income threshold — let’s say you’re earning $370,000 in 2024 as a married couple (just under the joint-filing limit of $380,100) — a $10,000 charitable contribution could bring you under the threshold, allowing you to claim the full Section 199A deduction.

Without that charitable deduction, you could be hit with limitations that reduce your total deduction significantly.

Example of a Benefit

Imagine you’re running a profitable business, and your total taxable income for the year is $390,000, which is over the Section 199A limit. Without doing anything, you might see your deduction cut down because you exceeded the income threshold.